André Ferraz @andreferraz91

https://t.co/X6diQn2fEM CEO and co-founder @weareincognia - fraud prevention for online businesses incognia.com Palo Alto, CA Joined October 2013-

Tweets785

-

Followers585

-

Following1K

-

Likes377

That's a robot. It's holding a real phone, typing into an app on its own. And in the video, you can see entire shelves of them. Fraud is entering its physical AI era. For years we fought automation as software: scripts, emulators, headless browsers, device farms. We got very good at catching those. Now automation operates real phones, taps real apps, and behaves through real-world interfaces, and that breaks a lot of assumptions. A CAPTCHA doesn't prove much anymore. A real device doesn't prove much. A human-like interaction doesn't prove much. These are pristine retail phones with real IMEIs and factory-standard operating systems. No root, no jailbreak, no emulator footprint for a security SDK to flag. A mechanical stylus does on real glass exactly what a human finger does. The stack itself is going physical. This makes fake account creation, promo abuse, payment fraud, mule onboarding, and account takeover much easier to scale. So the question changes. It's no longer "does this session look human?" It's "do the device, account, location, network, and behavior actually belong together?" That's where Incognia comes in. A hundred phones bolted to a shelf share one hyper-precise location. They never go home, never commute, never travel. They cluster at a density no real user base shows. Across a billion devices in 190+ countries, physical presence is the one signal these farms can't reproduce. We flag dozens of supposedly clean devices running from the same rack, and we know a real person moves through the world while a farm phone lives its entire life in a cage. As fraud becomes more physical, fraud prevention has to become more contextual. The next generation of defense won't rest on one challenge, one signal, or one screen test. It will rest on whether the whole relationship is real. Physical AI will make a lot of classic fraud defenses obsolete. Location identity isn't one of them.

Mule account handovers are increasing, they're crossing borders, and the people involved are often being coerced or manipulated. We surveyed over 500 fraud and risk professionals at financial institutions across the US and Europe to understand where the industry stands on this problem. → 81% report an increase in the last 12 months → 64% have suspected or confirmed cross-border cases → 72% say at least half of their cases involve some form of coercion or manipulation These are coordinated, global fraud operations. And a lot of the people caught in the middle are victims who don't know it yet. 53% say mule account handovers are harder to detect than other fraud types. And when you look at how they work, it makes sense. The account is real. The person who opened it passed KYC. The credentials check out. So when someone else starts accessing the account weeks later, the authentication system has no way to flag that the person has changed. Onboarding verifies who you are once. Authentication verifies that credentials are correct. Neither checks whether it's still the same person behind the account. Because of this, only 16% of institutions catch a handover before suspicious transactions occur. Most detection happens after the money has already moved. The industry is responding. 78% have made this a top priority for the next 12 months, but prioritization without the right detection layer just means faster response after the money's already gone. Full report: hubs.li/Q04kv7BR0

More features ≠ better solution. This vendor is known for having a lot of flashy features. A lot more than Incognia. But quality > quantity. Having a ton of features doesn't matter if they don't work. We don't try to do everything. We focus on a few things, and do them really well. DM me if you want to know which vendor this was.

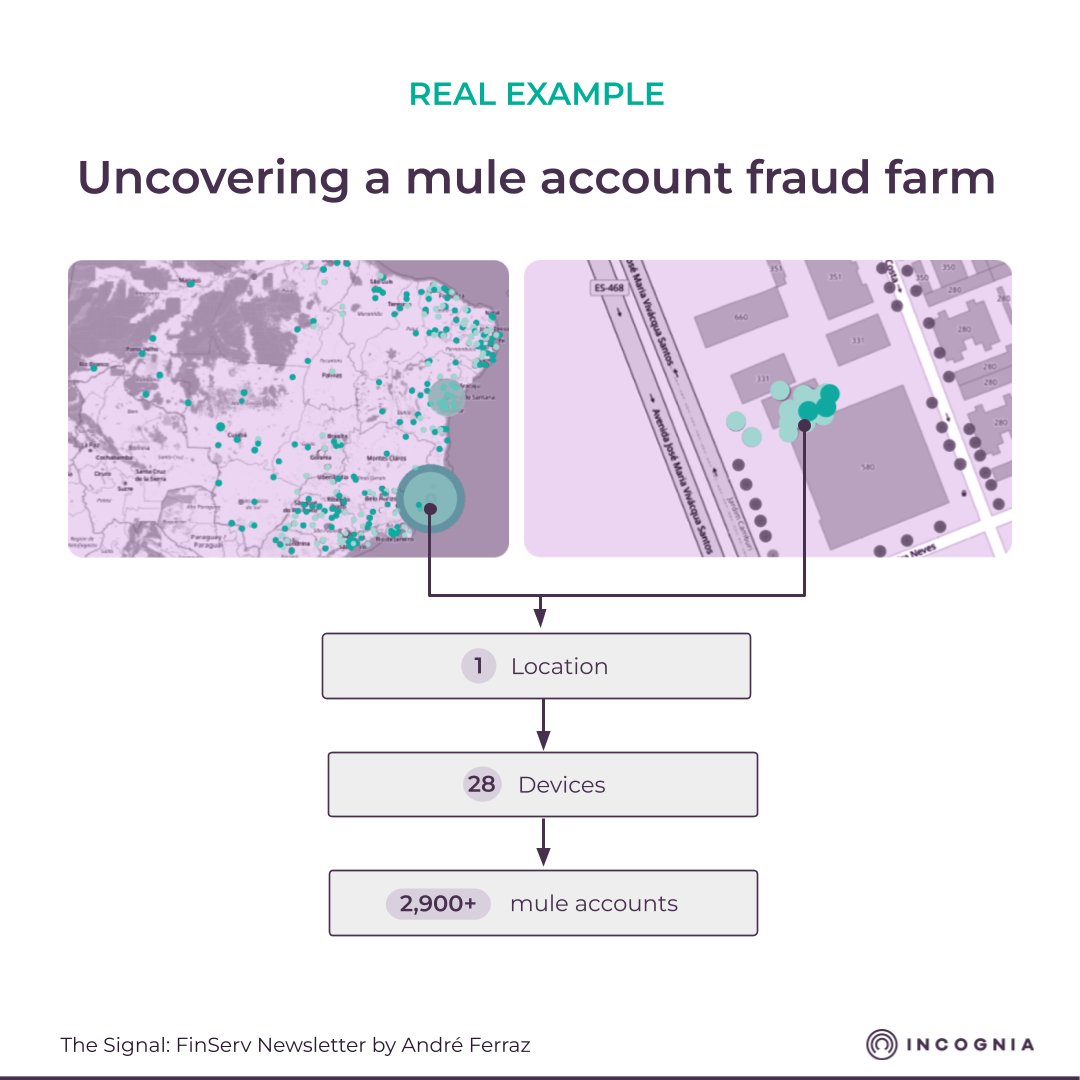

A bank had previously identified 11 mule accounts on their platform. When we ran a Proof of Value, we found over 2,900, linked to 28 devices, operating from one physical location. They couldn’t see 99.7% of their mule accounts. The difference between finding 11 and finding 2,900+ is the signals you're using and the quality of the data behind them. We were able to uncover these accounts by combining persistent device intelligence with precise location intelligence. Device IDs showed which devices were accessing multiple accounts. Location tied all 28 of those devices to the same physical place. The issue is that most institutions are using weak versions of both. In general, device IDs in the market are fragile. Browser updates, app reinstalls, factory resets can all cause a device ID to break and regenerate. When that happens, the same device looks new. The link between that device and the accounts it was accessing disappears. On the location side, most institutions rely on OS-level geolocation: GPS or IP addresses passed through by the operating system. IP only tells you what state someone is in. GPS can tell you the building, but not the unit. Without precise versions of both signals, there's no reliable way to tie the devices, the accounts, and the location together. And if you can’t find and stop mule accounts, you risk becoming criminals' favorite financial institution. — I go deeper on signal quality and how to evaluate your own signals in my newsletter. hubs.li/Q04ksd-t0

Social engineering is amateurs vs. professionals. End users are not fraud experts, and they're not going to become fraud experts. Social engineers are professionals. They specialize in putting the end user in an emotional state that will make them ignore whatever warning signs they're seeing. It's just a very unfair battle. Don’t put too much responsibility on your customers. It’s our job to figure out how to protect them.

Incognia says privacy-first fraud prevention gains traction in Europe biometricupdate.com/202605/incogni… via @BiometricUpdate

Catching mule account handovers is pretty straightforward. You just need the right data. The problem is that most institutions don't. Device and location intelligence are the right signals for detecting handovers. But in our State of Mule Account Handovers report, respondents ranked them as the leading sources of false positives. That tells me a lot of teams are working with weak versions of these signals. A new device ID on its own doesn't necessarily mean fraud. Device changes are normal. Over 100 million new devices are set up in the US every year. And web device fingerprints are fragile by design. Browser environments make device IDs unstable even when the device hasn't changed. On the location side, most institutions are relying on OS-level geolocation: GPS or IP addresses passed through by the operating system. This data isn't precise enough for fraud detection and is highly spoofable. VPN usage is common and not necessarily tied to fraud, so flagging every VPN user as suspicious just creates more false positives. Once you fix the data, the detection logic is clear. When a new login happens, there's a series of signals we look at: 1. Has the device ID changed? This is the starting point. But like I mentioned, a new device ID on its own doesn't mean much. People buy new phones. They switch browsers. A device change is a flag, not a conclusion. 2. Is the new device linked to other accounts? Whoever is managing mule accounts usually manages more than one.They need multiple accounts to launder money and funnel funds quickly. If the same device is tied to multiple accounts, that's a much stronger signal. But a sophisticated operator might use one device per account to stay under the radar. 3. Does the location behavior on the new device match the original? Not a single snapshot. The full history. If location behavior is consistent across both devices, it's probably the same person switching phones. But if there's a mismatch, that's a strong indicator that someone new is behind the account. 4. Have we seen other accounts at that same location? If a new device shows up and that location is already linked to other accounts, the picture gets very clear. Multiple devices, one location, all tied to different accounts. That's a very strong indicator of a mule operation. — None of these signals work well in isolation. But combined, with the right data quality behind them, they make handovers visible. I wrote about this in more detail in my most recent newsletter. Link to read: hubs.li/Q04j3Gj60

Incognia is now the most downloaded fraud prevention SDK in Europe. This is a big milestone for Incognia, and for the industry as a whole. GDPR pressure is forcing European banks and fintechs to rethink what data they actually need to collect to prevent fraud. For years, the industry has assumed that better security means collecting more personal data. More PII, more documents, more identifiers to verify "who" someone is. But now, companies no longer see privacy and fraud prevention as competing priorities. They want both. That’s why they’re choosing Incognia. We don't require things like name, email, phone number, or government ID to detect fraud. Instead, we evaluate whether an interaction is consistent with a device's typical behavior and location context, without trying to establish a person's real-world identity. And that’s how we've done it since day one. Our team is heading to Money20/20 Europe in Amsterdam next week. If you're rethinking your fraud stack, let's talk.

Porter had 4,500 overlapping multi-account orders per day. 29,000 unique partners contributing to the abuse in a single month. Driver-partners were cloning the app on a single device to run multiple accounts simultaneously. Accepting parallel orders from the same phone. How-to tutorials showing the exact technique on Porter's app were circulating openly on YouTube. Most of these were drivers exploiting a tech workaround to maximize earnings. Customers faced delays, and honest partners lost orders to those gaming the system. Porter wanted to stop the behavior at the source without losing active supply. Incognia's device intelligence was integrated directly into the Partner App, targeting the exact moment abuse occurs: when a partner taps "Go Online." When a second account tried to go live from the same physical device, Incognia detected the match and blocked that session. The GIF below shows this in action. The block was deliberate. Partners could still log in, browse the app, check earnings, access support. The behavior was stopped without cutting anyone off from the platform. Porter rolled it out city by city starting in December and hit 100% partner coverage by January. The results: ✓ ~80% drop in overlapping multi-account orders per day (4,500 to ~300) ✓ 10-15 support tickets per day from blocked partners out of ~5,000 active daily ✓ Zero wrongful blocks ✓ Zero downtime throughout rollout And on YouTube, the tutorials that used to show the exploit now have comments reading: "This doesn't work anymore."

One single Redmi Note 10S accessed over 400 accounts on a delivery platform and claimed nearly €2,000 in vouchers in 30 days. All they needed was an app cloner. These tools are freely available in any app store. A fraudster can download one, clone your app, and run multiple copies on the same phone. The more advanced ones take it further. The one in this video randomizes IMEI and spoofs MAC addresses, making each clone look like a completely unique device. Ten instances batch-cloned in under a minute. No technical skill required. From there, fraud scales fast. One phone can run dozens of accounts at once. This fuels a lot of common fraud types: → Promo abuse: every clone can claim new-user vouchers and promotions → Refund fraud: spread fraudulent refund requests across dozens of accounts so no single account looks suspicious → Ban evasion: get banned, spin up a new clone and device ID, come right back → Coordinated scams/collusion: control accounts on both sides of a marketplace and run fake transactions where no real order ever takes place The latest versions of these tools also include location spoofing, device ID spoofing, and fake camera feeds that let fraudsters upload deepfake videos to bypass facial recognition and liveness checks. If your device ID can't detect when an app has been cloned, none of these attacks are visible to you. The cloner, the fake accounts, the spoofed identities. Your system sees legitimate users. A lot of the teams we show this to have no idea these tools exist. But once they see their own app being cloned, it changes how they think about their entire fraud stack. — Can your platform detect an app cloner? We'll put it to the test for free. We'll run your app against a common app cloner tool fraudsters use and show you whether your current fraud stack stands up to the attack. Interested? DM me. We're running this with a select group of platforms.

My wife had her bank account taken over. Luckily, we caught it in time. But I was shocked at how easy it was to recover her account. In a bad way. 😬 I called from my phone. Different number than hers. Told the agent I was her husband. He immediately said I needed to hand the phone to her directly. Fair enough. She gets on. Confirms her date of birth and social security number. That's the authentication. The agent then reads her username back to her out loud for her to confirm it was correct 😮. After that, he asked to which phone number he should send the password reset link to, and that was it!!! Think about that for a second. If I wasn't her husband, I'd have owned that account in under five minutes. If I was a fraudster who'd bought her SSN and date of birth off a data broker, handed the phone to a woman, or used a voice AI to mimic one, I could have done exactly that. No technical skill required. No device exploit. Just social engineering and publicly available data. And that data is already out there. Credit reporting agency breaches. Merchant breaches. Bank breaches. SSNs and dates of birth aren't secrets anymore. Treating them like passwords is the real vulnerability. A fraudster used to have to execute these steps manually, one account at a time. That time requirement was the natural limit on how much damage they could do. AI is removing that limit. The same attack my wife experienced can now run in parallel across hundreds of accounts simultaneously. No extra headcount. No coordination overhead. Just an agent running the playbook on loop. Some fraud operations already have hundreds of people running scams full time. Multiply each of those individuals by AI-powered automation. That's where we’re at.

Just got back from Marketplace Risk in San Francisco. One thing stood out more than anything else: the disconnect between what the industry is focused on and what's actually hurting platforms right now. I'd estimate about 70% of the sessions and conversations were about agentic commerce. How agents will transact, what the fraud scenarios look like, how the chargeback rules will apply. I was part of one of those sessions. Agentic commerce is a real topic and it will matter. But it's not happening at scale yet. What became very clear across the sessions, and from conversations with banks and payment networks, is that there's still a lot to be defined. The rules around evidence for chargebacks on agentic transactions, liability, how disputes will work. None of that is settled. The transaction volume is still a tiny fraction of overall commerce. At the same time, refund abuse, promo abuse, multi-accounting, and chargebacks are happening at scale right now. And most platforms still haven't solved them. The part that concerns me is if a human can commit refund abuse or promo abuse easily today, automation only makes it scale faster. AI will amplify the fraud types that already exist. If you haven't fixed today's problems, you're not going to fix tomorrow's. Especially when tomorrow's problems are just today's problems running on better infrastructure. There's a lot of anxiety in the market right now about what's coming. I get it. But the companies that will be ready for agentic commerce are the ones solving today's fraud first. We're focused on both at Incognia. Solving what platforms are dealing with today while being ready for what's coming next.

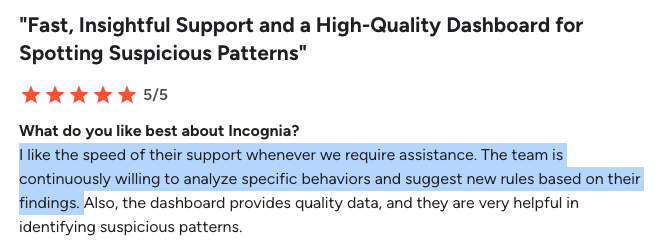

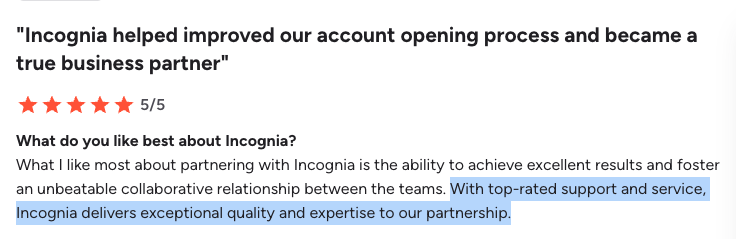

I've been noticing a lot of frustration from fraud and risk teams about their vendors' service models. The complaint is almost always the same: they charge for everything. Support, customization, analysis. Every request becomes a line item. We made a strategic decision early on at Incognia to include all services in the product. All of them. If we charge for services, then the team has an incentive to sell hours instead of improving the product. But if services are included, we're forced to keep making the product better so we spend less time on manual work. Problems that come up twice get automated. That's how the product improves. It also changes the dynamic with our customers. When there's no cost to asking for help, people actually ask. They send us edge cases, flag behavior they don't understand, push us on things they want to see. That feedback loop has been one of the biggest drivers of our product development. This is a big reason why we have 100% customer retention. We hear it directly from customers all the time. We have a 4.9 star rating on G2. I've attached a few reviews that speak to this. At Safeguard last week, some of our customers were in the room recommending Incognia to other companies evaluating device intelligence vendors. Unprompted. Based on how supported they feel. Hearing that in person meant a lot. We've worked hard to build this kind of relationship with our customers.

APP fraud passes every standard fraud control. On the surface, everything looks right: Trusted device ✓ Known location ✓ Valid credentials ✓ Legitimate user ✓ Authorized ✓ The fraud lives at the other end of the transaction. To catch it, you need to look at what's happening around the payment, not just the payment itself. Four signals worth watching: 1. Active call detection. Is the device on a phone call while the user is making a transfer? This combined with a new payee is a red flag. 2. New payee. Is this the first time the user is sending money to this account? New payee accounts are involved in 67% of payment fraud cases. 3. Mule account signals. This is the most important signal, and it requires FIs to collaborate. Has it collected funds from multiple victims? Is it connected to other flagged accounts? Was the account handed off? 4. Transaction size. A scammer isn't asking for $10. They're after serious money. Flag unusually large transfers, especially from accounts that have never sent amounts like this before. Armed with these signals, you can catch APP fraud before it's too late.

I've always been skeptical of behavioral biometrics. At Safeguard last week, I had the chance to talk with several companies that have deployed it over the past few years. The results have been well below expectations. Across the board. Some are exploring different behavioral biometrics vendors. Others are moving away from the technology altogether. The core problem is noise. Signals like keystroke patterns and phone angle change constantly. You're walking. You switch hands. You type with one thumb instead of two. Each of those changes looks like a different person to the model. False positive rates end up high, and legitimate users get blocked. Because the baseline is so noisy, every use case requires extensive fine tuning. That tuning takes years. And by the time the models are calibrated, the attack patterns have changed. Fraudsters adapt faster than the models can keep up. One example I've referenced before: a major bank spent roughly $10M/year on a behavioral biometrics vendor. → Year one was just sending data so models could be trained → Year two, more training → Year three, they finally went live and performance didn't meet expectations → Year four, they canceled the contract. The vendor handled bot attacks reasonably well, but the majority of attacks were manual. And manual attacks look like normal user behavior. That's where behavioral biometrics breaks down. The victim in a social engineering attack types normally. Swipes normally. Holds the phone normally. The behavior is indistinguishable from a real user because the person is a real user. If the industry is going to use this technology, it needs to set the right expectations. Behavioral biometrics is a risk signal. Treating it as an identity solution is where companies get burned.

Mule account handovers create two problems at once. 1. The fraud side: the account passed KYC clean. The right person opened it. But when someone else starts using it weeks later with the right credentials, the system has no way to flag that the person behind the account has changed. Onboarding and authentication are often separate processes. Different teams. Different vendors. Different signals. Neither checks whether it's still the same person. 2. The CX side: mule account handovers trigger more false positives than other fraud types. And the most common response is to lock the account down. When false positive rates are already high, legitimate customers get caught in it. Accounts frozen. Payments blocked. People who didn't do anything wrong get punished. So the fraud problem becomes a customer experience problem, and now you’re trading fraud losses for customer friction. — I wrote about this in more detail in my new newsletter. I also break down what we found after surveying 500+ fraud and risk professionals across the US and Europe on where the industry stands with mule account handover detection. Read it here: hubs.li/Q04fQ24P0

I get to see firsthand what fraud teams are up against inside leading banks and fintechs. I see what's working, what's failing, and what's coming next. Most of that never makes it into a LinkedIn post. There's too much context, too many details. So, I’m launching a newsletter specifically for fraud and risk professionals in financial services. You'll get: → What's changing in fraud and how practitioners are responding → Real cases showing how specific fraud types play out and how they get caught → Observations from conversations I'm having with fraud teams every week → Original research and data from the field Mule accounts. Account takeover. APP fraud. RAT scams. Social engineering. AI-enabled fraud. All of it. The first issue drops soon. Subscribe here: hubs.li/Q04fqg4V0 What fraud problems are you spending the most time on right now? I want to make sure we're covering what matters most.

Webull Brazil used a fraud heat map to change where they spend their promo budget. When Webull launched in Brazil, they grew fast. Promotional campaigns were driving user acquisition. The problem was what came with them. Bonus abuse. Account sharing. People opening accounts just to withdraw promo funds and disappear. Traditional verification added friction for good users without catching coordinated abuse. Once they implemented Incognia, we quickly saw the scale of the problem. 571 devices were operating in coordinated promo abuse networks. 1.5% of accounts in our database were shared by two or more devices, with critical cases showing four or more distinct devices per account. The heat map showed exactly where it was concentrated. We could see the specific regions where multi-device account sharing was systemic. Webull used that intelligence to pull campaigns in high-risk areas and redirect budget toward markets that were actually converting real users. The onboarding experience for legitimate users improved, too. Moving from manual to automated verification pushed the low-risk approval rate from 75.7% to 92.5%. Manual review dropped from 19.2% to 2.5%. Real customers stopped waiting. And then a finding we weren't specifically looking for: 7,650 devices showed active remote access tools like AnyDesk and TeamViewer. Primary tools used in RAT scams targeting investors. Webull was able to act on that before it became a loss event. When you can accurately see where fraud clusters, you stop spending money acquiring it.

GPT-5.5-Cyber rolled out this week. Claude Mythos came out last month. Both models can find software vulnerabilities, write working exploits, and reverse-engineer compiled code at a level that used to require years of specialist training. Defenders benefit from this. Attackers benefit more. The same model that helps a SOC analyst triage faster lets a fraud operator spin up convincing phishing pages, synthetic identity stacks, and deepfaked video on a laptop overnight. What AI doesn't solve is identity. If digital deception is now cheap and abundant, everything the industry has been calling "identity verification" needs to be rethought. Passwords were already broken. SMS OTPs have been broken for years. Document scans and selfies are spoofable by anyone with a free model checkpoint and a weekend. We've been making this argument since we started Incognia: identity has to be grounded in the physical world. Not as a marketing line, but because it's the only signal class that doesn't collapse the moment generation gets cheap. Where a device actually sleeps at night. The WiFi networks around it on a Tuesday morning. Bluetooth peripherals it's been paired with for the last six months. Which cell tower it hits when it leaves for work. You can't fabricate a year of that. Not with a frontier model. Not with a deepfake studio. Not with a residential proxy. The companies that come out ahead in cybersecurity over the next decade won't be the ones with the best models. They'll be the ones sitting on data no model can synthesize.

Tiago Lima @fltiago

223 Followers 439 Following

Porto Digital @porto_digital

41K Followers 406 Following O principal distrito de inovação da América Latina, impulsionando tecnologia e inovação há mais de 24 anos.

CIn-UFPE @CInUFPE

8K Followers 507 Following Canal oficial do Centro de Informática da UFPE no Twitter. Visite também: Instagram: @cinufpe Linkedin: @cinufpe Medium: @cinufpe Facebook: @CInUFPEOficial

Márcio Bonfim @bonfim_marcio

70K Followers 450 Following Pai da Sarah, Miguel e Mateus, filho da dona Helena, marido da Mari, paulista, mineiro por adoção, pernambucano de coração, jornalista e apresentador

Dudu Rocha @dudurocha

759 Followers 499 Following I build products and solve problems at YouTube. Looking for the best cheese and natural wine in Paris 🇫🇷. From Pernambuco, Brasil.🇧🇷

rods 🌦️ @RodsFarias

156 Followers 300 Following Tweets pra vc pensar "Ta, ninguem liga" e rir da minha cara

inumaginfo.com @inumaginfo

2K Followers 5K Following Magazine d'info/Actualité - Osez l'INFO avec un autre regard, auto-produit, libre et indépendant (reportages vidéos...) G.Liaboeuf E.Fongarnan - @inumaginfo

Adir Shemesh @ShemeshAdir

5 Followers 1K Following

Horia Adamov @horiaadamov

6 Followers 280 Following QA Automation Architect | I Build Bulletproof Frameworks That Slash Release Times & Deliver Rock-Solid Software Confidence

Number Play @numberspla93353

158 Followers 2K Following

Affordable Decor Idea... @Decorsforlove

1K Followers 4K Following The latest trends and innovative ideas to transform your living space into a comfortable and stylish home. Daily Amazon product links with over 4.5 ⭐ ++

Goldie @GoldieLeGenie

155 Followers 465 Following

𝐒𝐭𝐞𝐯𝐞 ... @stevechenz

8 Followers 202 Following

NydiaColclough @fe6U89724sr4u27

164 Followers 6K Following Wanderlust warrior collecting sunsets and passport stamps

Florine Emard @FlorineEma40799

134 Followers 5K Following

David Nesbitt @daviddangern

306 Followers 377 Following Some funny tweets, some serious ones too ☺️ follower of Christ, husband, boy dad. I love music, books, peanut butter, coffee, content marketing, humor.

CurvyTeacherChloe ✨ @denver_chloe28

59 Followers 1K Following Hiking & iced coffee. 3rd grade teacher ready for some adult fun.

Rodrigo Borges @seoborges

581 Followers 620 Following Entrepreneur and Internet startup investor. Co founder of https://t.co/LVj66fw2Wl and now partner at https://t.co/4eCyDEhiC9

AmandaWallace @mezokuse1986

33 Followers 599 Following

Ruvo @ruvopay

378 Followers 195 Following Faça sua transferência. USD para BRL em segundos. Taxa mínima, com segurança, sem IOF e direto no PIX.🇺🇸🇧🇷 📍 @ycombinator

COACH GAVIN @SamuelKiyae

48 Followers 668 Following I test, review, and recommend only the most valuable products and services that I personally use to build my passive income streams. No fluff, just results.

FredaFowler @4vnmf2n74z744

34 Followers 1K Following

Elina Ma @99dabaicai99

12 Followers 153 Following

Gustavo De Mari Perei... @guhdemari

457 Followers 6K Following machine learning, data science, software engineering

Sliexu @Sliexu8114

9 Followers 762 Following

Carli Roob @carli13128

30 Followers 2K Following

Adalberto Brandão @BetoBrandao

606 Followers 2K Following Founder & CEO @scoutfy all about Sports, Sports Science, Sports Tech, Design, Digital Health, Tech Startups, VC, Angel Inv., Entrepreneurship.

Victoria Wren | Digit... @VWRen_Official

23K Followers 12K Following Co-Founder SPREAD | Driving ecosystem growth with @ethereum, @HarvardBiz, @CoinDesk, @TechCrunch & @Cointelegraph | Digital Strategy & Influence Architect

Nasepha @NasephasLaL42B

57 Followers 2K Following

Álvaro Rossi @alvarobrossi

47 Followers 461 Following

Teshoadr @teshoadr21603

8 Followers 298 Following

Kahue Cardoso @KahueCardoso

219 Followers 603 Following Ecomm, Fintech, Risk, Fraud Prevention and Identity

Jeff James Martin @lead_by_change

1K Followers 2K Following Building Peak OS - the operating system for modern teams @empower_change | Author - Peak Teams | Producer - Tech Scenes | 3x Founder | BJJ Black Belt

jccl @celso_jccl

6 Followers 147 Following Software Developer Node, Go, React https://t.co/CUE0DeR8zz https://t.co/aAutRDurpq

Felix Jeremiah @FelixJeremiah12

3 Followers 109 Following Solving problems with code and caffeine ☕💻

ChloeTout @7TS11V1o24W3Ep

61 Followers 7K Following

Teetirez @TeetirezBXIM

43 Followers 4K Following

XantheAdams @bt6cCV7ZnKF7R

62 Followers 7K Following

Slisioez @Slisioezkn1cCt

45 Followers 3K Following

Sotetee @SoteteeyQ92I

12 Followers 1K Following

big_bets @bigbetstech

5 Followers 243 Following

tiagaohanasac @tiagaohana3421

2 Followers 13 Following If awaking from greater offenders are pressed.

Paul Tseluyko @paultseluyko

538 Followers 642 Following Building: @thecapableio - the ultimate prompt tool for B2B ⚒️ / @Merge_Dev - UX agency for startups 🤖

Loallee @Loallee180735

88 Followers 7K Following A strong woman is one who is determined to do what others are determined not to do.

lily @V083SZ3fbAO8a2m

83 Followers 7K Following

Pislaret @pislaret64741

75 Followers 7K Following

silvio meira @srlm

147K Followers 365 Following founder: https://t.co/dRezX3Tv2Q, https://t.co/XBZdjugRgR, https://t.co/AOImgfKEj1, https://t.co/CxlJgi9BhW, https://t.co/VaBIuzm9V4, https://t.co/R3qQLbtjJ4.

Tiago Lima @fltiago

223 Followers 439 Following

Andrew Gazdecki @agazdecki

311K Followers 7K Following Founder and CEO of @acquiredotcom. https://t.co/wRMIssDmhl has helped 1000s of startups get acquired and facilitated $500m+ in closed deals.

CIn-UFPE @CInUFPE

8K Followers 507 Following Canal oficial do Centro de Informática da UFPE no Twitter. Visite também: Instagram: @cinufpe Linkedin: @cinufpe Medium: @cinufpe Facebook: @CInUFPEOficial

Dudu Rocha @dudurocha

759 Followers 499 Following I build products and solve problems at YouTube. Looking for the best cheese and natural wine in Paris 🇫🇷. From Pernambuco, Brasil.🇧🇷

Henrique Dubugras @hdubugras

106K Followers 283 Following Proud Brazilian in Silicon Valley. Co-founder and Chairman @brexhq

Brian Halligan @bhalligan

106K Followers 2K Following Co-founder HubSpot | Sequoia | Propeller | MIT Host, Long Strange Trip pod: https://t.co/qj9yOQVYaU

David Marcus @davidmarcus

197K Followers 1K Following CEO & co-founder @Lightspark ➡️ building the open Money Grid on Bitcoin + @spark. Ran Payments/Crypto & @Messenger at @Meta, led @PayPal + 3 startups.

Ethan Choi @EthanChoi7

8K Followers 5K Following prev @Khoslaventures, @Accel /views r my own. wrk w/ @OpenAI, @ClickHouseDB, @glean, @vercel, @tryRamp, @AbridgeHQ, @R1RCM, @Anrok, @dualentry, outsmart

Cory Levy @cory

151K Followers 4K Following entrepreneur and early stage investor | Z Fellows @zfellows

Daniel Gross @danielgross

236K Followers 0 Following

Dave Morin 🦞 @davemorin

492K Followers 4K Following Founder @OfflineVentures @Slow @Path • Chairman @Esalen • Board @OpenClaw • Early @Apple @Facebook • Podcast @MoreOrLessPod • Skier • Dad of 3

Mustafa Suleyman @mustafasuleyman

627K Followers 496 Following CEO, @MicrosoftAI | Author: The Coming Wave | Past: Co-founder, @InflectionAI & @GoogleDeepMind

Eric Glyman @eglyman

180K Followers 2K Following Co-Founder at Ramp (@tryramp). New York City. Previously co-founded Paribus (Acq. by Capital One).

Siqi Chen @blader

251K Followers 4K Following 🏗️ Love to build (@runwayco @sandboxvr @zynga) people love 💸 Investor @mercury @owner @elevenlabsio @meetgamma @sfcompute @turingcom @recallai @eightsleep ++

Kulveer @kul

123K Followers 4K Following Visiting Partner @ycombinator. Backing high-output YC founders via @phosphorcap. Previously founded and sold @ZeusLiving (S11) & @auctomatic (W07).

Tom Preston-Werner @mojombo

58K Followers 4K Following Inventor. Investing @PWVentures. Formerly: GitHub cofounder. Board @HackClub @Ona_hq @MoteHydrogen. Also: Gravatar, Jekyll, SemVer, TOML, RedwoodJS.

Lachy Groom @lachygroom

137K Followers 906 Following it's pronounced locky. [email protected]. π.com

clem 🤗 @ClementDelangue

399K Followers 5K Following Co-founder & CEO @HuggingFace 🤗, the open and collaborative platform for AI builders

Jon Oringer @jonoringer

135K Followers 2K Following Founder of Shutterstock. Spinning up agents, building network effects, and skipping permissions.

Jaynit @jaynitx

54K Followers 108 Following Building aHQ | Helping VCs & founders to build an unforgettable Personal Brand | Writer • Thinker • Self-Improvement

NWS Bay Area 🌉 @NWSBayArea

235K Followers 661 Following Official Twitter account for the National Weather Service San Francisco Bay Area. Details: https://t.co/ASDrLwF1Yj

Rachel Tobac @RachelTobac

113K Followers 8K Following Friendly Hacker & CEO @SocialProofSec security awareness/social engineering prevention Training, Videos, Talks | 3X @DEFCON🥈| Ex CISA gov Tech Advisory Council

briankrebs @briankrebs

331K Followers 2K Following Independent investigative journalist. Author of 'Spam Nation,' a NYT bestseller. Former Washington Post reporter. Mastodon: https://t.co/fTKNavlMwp

Troy Hunt @troyhunt

249K Followers 1K Following Creator of @haveibeenpwned. Microsoft Regional Director. Pluralsight author. Online security, technology and “The Cloud”. Australian.

Jim Browning @JimBrowning11

166K Followers 195 Following I can't stand scammers, so I try to do something about them. Awareness is key, so I have a YouTube channel exposing them and their scams.

Kitboga @Kitboga

123K Followers 159 Following Improv artist who calls scammers & explores the internet. Laughter is the best medicine. https://t.co/aEC5M10HUJ Business Inquiries: [email protected]

Pierogi @ScammerPayback

120K Followers 165 Following Come join us as we go on the adventure of giving visibility into scammers and how they operate. [email protected] (Business ONLY, no investigations)

Avivah @avivahl

2K Followers 147 Following

Shawn Carolan @shawnvc

4K Followers 771 Following Investing in consumer tech to make life better/faster/cheaper @Menloventures. Founder, engineer, product fanboy, dad, aspiring empath, and in ❤️ w @jencarolan

Morning Brew ☕️ @MorningBrew

581K Followers 2K Following Everything you need to know about the world of business and the business of the world. ☕️

JD Vance @JDVance

5.5M Followers 1K Following Christian, husband, dad. Vice President of the United States.

Donald J. Trump @realDonaldTrump

111.7M Followers 53 Following 45th & 47th President of the United States of America🇺🇸

Catherine Herridge @C__Herridge

1.0M Followers 59 Following Emmy winning investigative journalist. Telling the stories I could not tell before, where the facts have a power all their own. #CatherineHerridgeReports

Prof. Feynman @ProfFeynman

1.4M Followers 0 Following A universe of atoms, an atom in the universe. Tribute to the great explainer. Tweets about Science and Wisdom. Portrait by L.V Patten.

thiswontlast @thiswontlast

362 Followers 8 Following Podcast: @rabois + @loganbartlett + @kevinryan + @zachweinberg Part of @turpentinemedia

Vivek Ramaswamy @VivekGRamaswamy

3.6M Followers 306 Following Father. Husband. Entrepreneur. Candidate for Governor of Ohio. Posts made by Vivek’s team.

SpaceX @SpaceX

41.9M Followers 123 Following SpaceX designs, manufactures and launches the world’s most advanced rockets and spacecraft

Forbes Technology Cou... @ForbesTechCncl

15K Followers 4K Following #1 vetted professional networking community for leading CIOs, CTOs and senior technology executives. Official partner of @Forbes. Membership by application.

Neuralink @neuralink

1.8M Followers 1 Following Creating a general-purpose, high-bandwidth interface to the brain

Joseph Cox @josephfcox

91K Followers 3K Following Hacking/crime/privacy journalist. Author of DARK WIRE. Co-founder of @404mediaco. Signal: joseph.404 Email: [email protected]

Thiago Alvarez @thiago_alvarez

148 Followers 883 Following Entrepreneur. Creator of Open Banking in Brazil. Guiabolso Founder (sold to PicPay); Angel Investor; living in Hawaii

Jack Altman @jaltma

235K Followers 618 Following Partner @Benchmark. Previously founded Alt Cap and Lattice.

Gabriel Vasquez @GEVS94

5K Followers 2K Following AI Apps + Global Investor @a16z | Future King of 🇸🇻, First of His Name | God chose the foolish things of the world to shame the wise - 1 Cor. 1:27

Eric Kaplan @eric_kaplan_nyc

407 Followers 2K Following Investor at @BessemerVP | Previously growth & product @ridewithvia | Seinfeld enthusiast ericnyc.eth

You might like