Quant Beckman @quantbeckman

Quantitative Researcher & Dev. | Financial Data Scientist | Machine Learning Engineer | Mathematical Research | Algorithmic Trading Systems quantbeckman.com Fresh takes on Quant Research Joined July 2019-

Tweets4K

-

Followers12K

-

Following0

-

Likes844

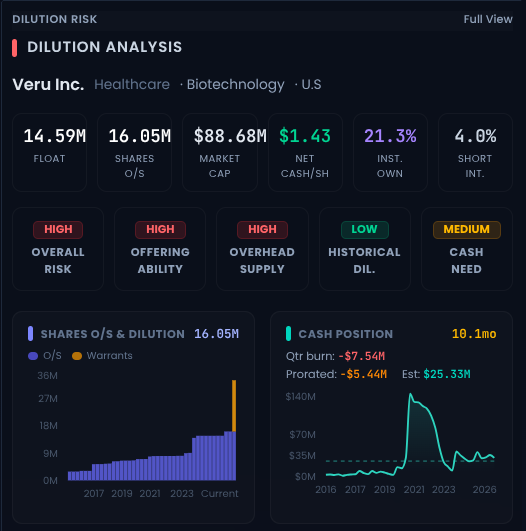

$VERU 144% It's a hairy candle, it looks like dynamite... so check in more detail here

📘[QUANT LECTURE] Quality standards of a strong hypothesis📘 👇👇👇

🟥For this one and more papers with code: quantbeckman.com

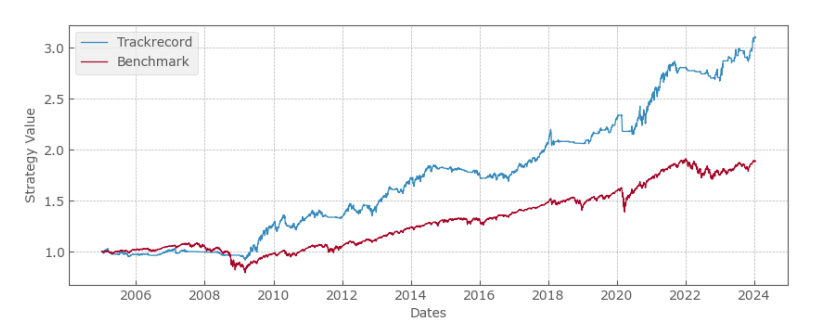

Risk-off strategies often look good because they avoid a few large drawdowns (2008, 2020, 2022)

Trading has 2 complementary legs and for some reason a lot of people focus only on one of them

Vol-of-vol can move before spot volatility fully reprices. When VVIX jumps faster than VIX while front VIX futures lag, the options market may be pricing a convexity shock before the futures curve catches up. Buy defined-risk VIX call spreads to express that convexity repricing without unlimited premium exposure. Exit when VVIX mean-reverts while VIX remains elevated or when the futures catch-up has already occurred.

🟥For this one and more papers with code: quantbeckman.com

The graph construction is depends on Pearson correlations estimated from 125-day windows, and more than 5 parameters. Small changes in these design choices reorder centrality rankings and therefore change the selected stocks. So the results are pretty unstable.

One of the most used phrases in quantitative finance: "correlation ≠ causation"

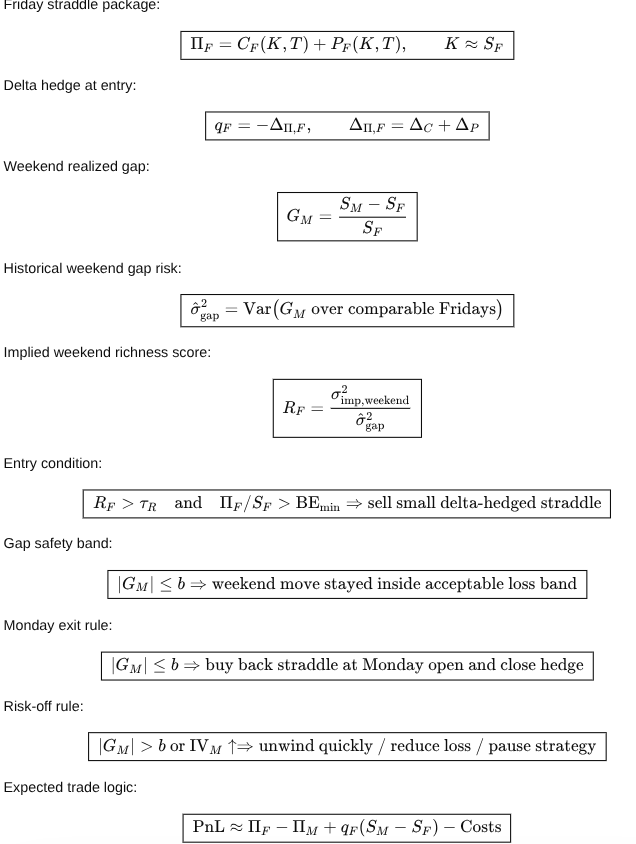

Equity-index options often price weekend uncertainty through implied variance, while realized Friday-close to Monday-open movement may be smaller in quiet regimes. The trade sells a small delta-hedged index straddle near Friday close when implied weekend variance is rich. The position is bought back Monday open if the realized gap stays inside a preset band. The edge is weekend theta capture, but the risk is jump exposure while markets are closed.

🟥For this one and more papers with code: quantbeckman.com

The authors show that performance is highly sensitive to noise, and bottleneck size. Once Gaussian noise rises beyond around 5%, or the bottleneck becomes too large, the Information Ratio declines.

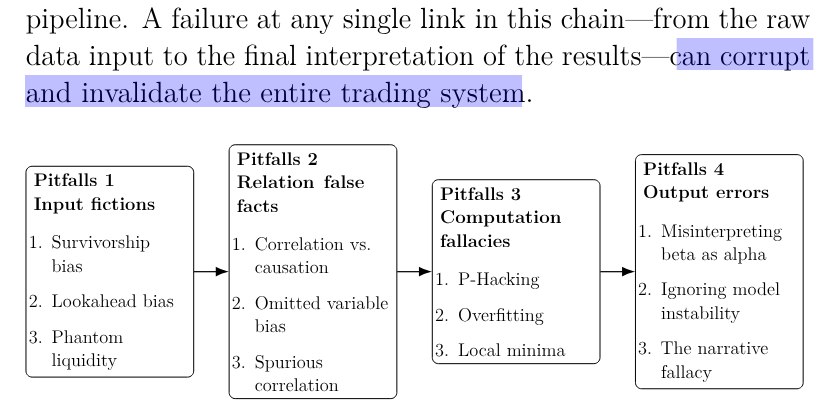

These are basically the pitfalls I look for every time I read a paper, and in this same order.

@algotrading_ios Hey man! I should develop this idea more but this are mere notes. If I have to choose, the simplest is: median Hajahahahah

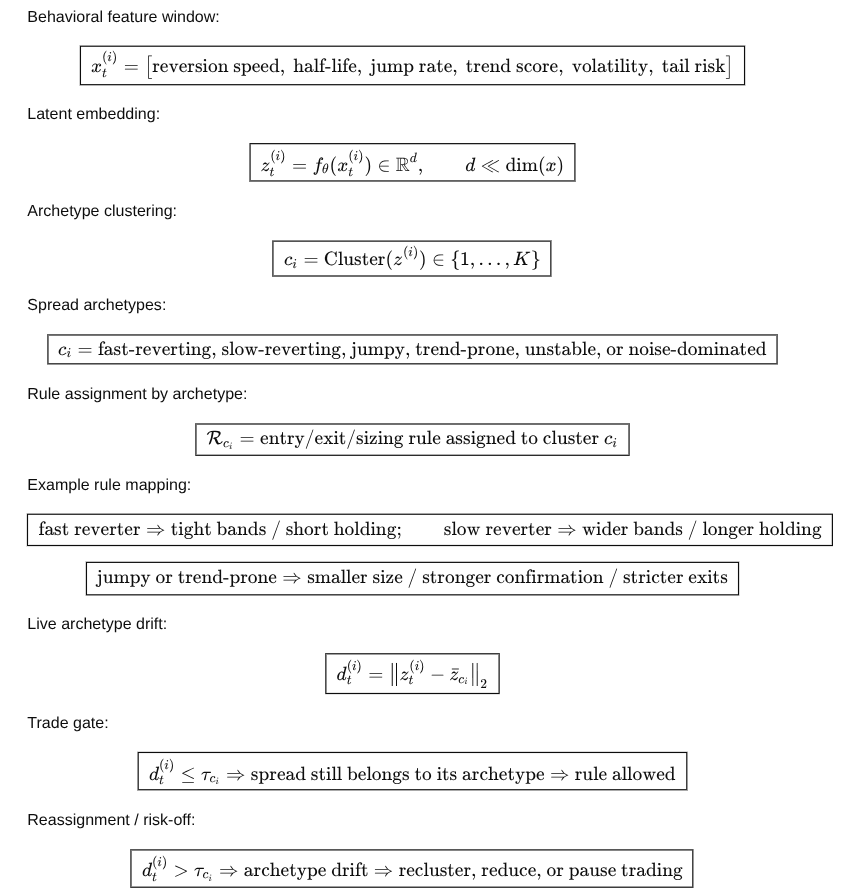

Some spreads revert fast, some revert slowly, some jump, and some trend after breaking. Embed each spread into a latent space using features or sequence encoders that capture its behavior over time. Cluster the latent points into archetypes, then assign trading rules suited to each cluster.

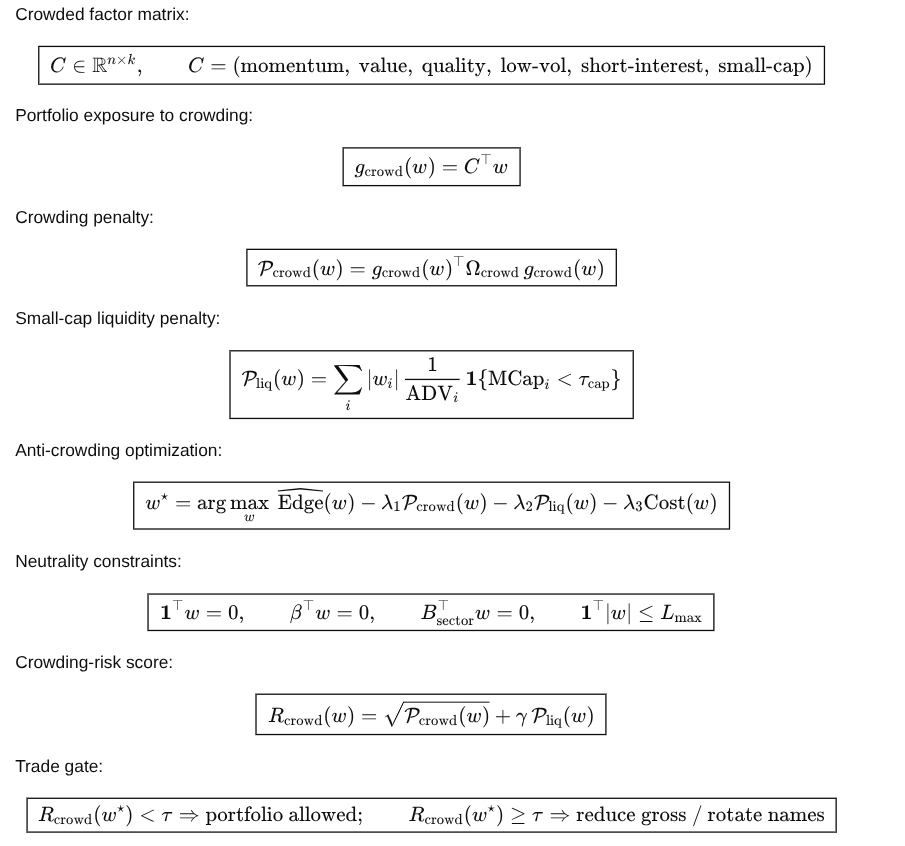

Some factors can unwind together when liquidity disappears, especially in small caps. Build a portfolio objective that rewards expected edge but penalizes exposure to known crowded factors.

🟥For this one and more papers with code: quantbeckman.com

The supervised stage trains the DDPG actor to imitate Markowitz allocations. The problem is that Markowitz weights are extremely sensitive to expected returns and covariance estimates. Atiny estimation error can produce a large change in weights

Each state represents a market environment where mean-reversion sleeves may behave differently. Instead of running MR continuously, estimate which latent state is active today. Only allocate to MR sleeves in states where historical survival and drawdown are acceptable.

Ralph Sueppel @macro_synergy

18K Followers 410 Following Managing Director of Macrosynergy. Development of systematic macro trading strategies.

SpreadGreg @optiongreg

9K Followers 1K Following Gestor +11 años Derivados+Vola+Spreads+Padre de Familia. Tweets no recomendaciones https://t.co/gOU6keGwP4 https://t.co/7KmW0wTJv5

Gerard @Gsnchez

27K Followers 568 Following Programando en BQuant. Prof. MSc in Finance @bsm_upf, MEF @unav. 🎬 https://t.co/3IFs5Ae0Wq

X-Trader @XTraderdotnet

6K Followers 1K Following Portal y comunidad para traders. Todo sobre estrategias de trading y mercados financieros.

MKTSignals | Inversio... @mktsignals_org

3K Followers 311 Following Herramientas para tomar el control total de tus inversiones: #AmplitudDeMercado, #Amibroker, #Sistemas, #BaseDatos, Alertas de #MarketTiming y mucho más.

Artur Sepp: Systemati... @ArturSepp

10K Followers 336 Following All views systematic: https://t.co/hz2IJAhW7R & https://t.co/mGbPf9PtMf. Quant of the Year by Risk Magazine: https://t.co/7MeiDASJc2

SERSAN SISTEMAS @sersansistemas

5K Followers 672 Following 📊 25 años en trading 🤖 Sistemas en real (SYO+OYS) 📉 Sin método no hay consistencia 🎯 Empieza a automatizar ↓

QuantpTrader | Robust... @QuantpT

3K Followers 281 Following Robust algo trading Edges for traders using AmiBroker & EasyLanguage. For serious traders focused on risk, robustness & realism.

Ivan Scherman, CMT, C... @IvanScherman

60K Followers 1K Following CIO at https://t.co/eTgt1vPj4z Winner of the 2023 World Cup Championship of Futures Trading. Awarded as Best Audited Trader 2023/24 by Rankia.

Sergi de Sersan @SergiSersan

4K Followers 3K Following Trader pro +20 años con track record público. Opero cada día con sistemas reales. Ahora enseñando trading algorítmico para que ganes con datos, no con emoción.

Juan Romero 📊 Quan... @quantforall

2K Followers 230 Following Inversión cuantitativa. Opero con mi dinero y te muestro las operaciones Para ver los sistemas suscríbete ⬇️ 📧 Newsletter 👉 https://t.co/JNznLsxcYv

Hobbiecode @hobbiecode

724 Followers 134 Following 📈Trader Algorítmico. Emprendedor. Make your life easier.

Rubén Martínez @rubenmesteban

8K Followers 500 Following Trader Algorítmico. Top 5 Campeonato del Mundo 2025.

Quantocracy @Quantocracy

24K Followers 196 Following Curated links from the quantitative trading blogosphere.

José Suárez-Lledó @SuarezlledoJ

4K Followers 700 Following Fondo Global Gradient | Bissan Wealth M | Moody's Analytics, PhD UPenn | Teaching @ Pompeu, IESE, ESADE. Finanzas, Economía, Aprendizaje, Problem Solving

Mariano Volpedo @marianovolpedo

2K Followers 918 Following Escencialmente. Teorico del Trail. Algo de trading. Quantamental. Dueño de El Cielo. Cosas que vuelan tambien. No me pidan coherencia, voy aprendiendo.

Andy备忘录 @Andydisobey

2K Followers 2K Following X首席评论官:我先评,你随意。 保守主义 | 财经时政 | 美股投资 | AI学习 CPA | 前四大审计师 Non-PhD

Jean-Cédric Favre @JeanCdricF67437

1 Followers 54 Following

xywl @_xywl

88 Followers 139 Following

Mikey Bravo @mikeybravogainz

4 Followers 34 Following Market-moving news dealer 💸 My analysis hits harder than your margin call. 🧠 Stay hedged, stay based. Faster than your algo, cooler than your PM. 📉📈

bil mor @mor_bil

58 Followers 2K Following trading since 1987…ex-Nymex, ex-London, ex-Europe, ex-Htown, ex-MT...

Fatih Aydemir @fthydmr

762 Followers 645 Following Quant @OpesBorsa | e/acc | #War | #Debt | #FX | #Gold | #Bitcoin | Formerly 🇪🇺ZEW, 🇬🇧LSE, 🇩🇪MA, 🇳🇴NHH, 🇦🇹Erste

玄投君 Flame @Evan99503

368 Followers 235 Following 想搞懂世界怎么运转。 用代码造工具,用不对称博弈,用术数看世界。 https://t.co/nQMgmfXgCT

Nik Kraner @NiikKraner

25 Followers 155 Following

onlygame @onlygame0

19 Followers 283 Following

eagleneddle @eagleneddlead

0 Followers 2K Following

سوبر ترند ل�... @SuperTrendMy1

17K Followers 763 Following نقدم دورات تدريب على برنامج سوبر ترند وهو برنامج حاسوبي يعمل كأداة تصفيه وماسح فني آلي بالمعادلات الرياضية و بالذكاء الاصطناعي للاسهم السعودية والامريكية.

Tanzwut @tanz6677

0 Followers 11 Following

naeya :D @HEROINAEYA

8 Followers 35 Following looking for moots who are interested in finance and stocks!

🐶 @modice568

110 Followers 907 Following

Albero Marafatto @AlbertoMaraf

4 Followers 54 Following

hobart @hobart24928224

203 Followers 6K Following Our hearts are all yearning for something indescribable

Moka @Moka34257573

54 Followers 834 Following

Ra Endymion @Custodian_Ra

413 Followers 381 Following

Papirosa | Algo Labs @AlgoPapirosa

31 Followers 21 Following

Riskfolio-Lib @RiskfolioLib

21 Followers 9 Following Portfolio Optimization in Python, easy for everyone

Pranav Mahajan @PranavMaha35061

13 Followers 39 Following

tradr @chadtradr

9 Followers 85 Following

Algorand @MrPisoul

17 Followers 106 Following #INTP Automated trading system architect and algorithm engineer at a fund, coding in: Cpp, Python, Rust, C#, Golang, Vue & React, R, etc.

Kokokocorn @kokokocorn2026

499 Followers 4K Following #Finance #realestate #foodtours #physics #math #politics #demographics #DNAmysteries #soccer #Sakatsuku #scenery #art #DokkanBattle #reading #AI #Thinking😎🌈

Frama @frama444

262 Followers 409 Following Lic en Finanzas | Finanzas Quant UCEMA | Quantitative Trader | Knickerbocker

ConvexityEgg @ConvexityEgg

3 Followers 31 Following

Rauf Muradlı @MuradlRauf

16 Followers 162 Following

Nuch @BitNuch

9 Followers 184 Following

VaporTrader82 @VaporTrader82

126 Followers 895 Following Aviation Worker and Aerospace lover. Futures Trader. Flight Simulation enthusiast & Kind of gamer.

Eddy @EddysForge

12 Followers 112 Following I am the sheep that got lost; fortunately for me, I was never found.

Kewal Talele @thor_4162

0 Followers 40 Following

Graber @GraberSwiss

77 Followers 674 Following

Ivan Ganev @ivanganev98

21 Followers 655 Following

arnold irangi gideon @gideonirangy

324 Followers 2K Following

You might like