Merchant Seven @MerchantSeven

M7 is the first of its kind FDE firm for financial technology. We invest in early-stage trading technology companies and scale the rest. merchantseven.com Here Joined September 2022-

Tweets138

-

Followers52

-

Following9

-

Likes119

The clip is old. The thesis is current. A little more than 2 years ago, Pierce Crosby, then advisor to TradingView, said something that nobody was paying attention to. He was describing, in 2024, what is happening in the prop trading industry right now. The prop industry did not grow because retail traders suddenly got better, it grew because the model has become structurally superior: lower barrier to entry, asymmetric upside for the participant, and a revenue engine that did not depend on client profitability. Brokers have noticed, and many are involved now, not as challengers, but as the infrastructure owners. That transition is what our Retail Prop Trading Report maps out full, in two editions. Part II is now live on site as well.

The retail prop firm playbook has a mathmatical advantage on the brokerage market: In the traditional brokerage (e.g., XP Inc., @CharlesSchwab, Pepperstone), a broker spends anywhere between $300 and $1,500 (CAC) on marketing to acquire a retail trading clients. During volatile periods large chunks of of these clients blow up their account within 3 to 6 months. LTV often doesn't cover the CAC. The broker loses money or breaks even at best. The prop trading model reverses this equation. Clients PAY to enter the account funnel. Across the category, the average client pays anywhere from $50 - $100 to take an evaluation challenge > The prop firm immediately recognize that revenue. Negative CAC. Evaluations filter out bad traders, and in the end, the broker is left with a qualified set of customers, educated by the process, who has already generated revenue even before making their first real trade. If they fail, they receive a performance report (often powered by AI) explaining where they went wrong. They learn. They try again. This is not fiction. It's loyalty through education, instead of promotion. @MyForexFunds and @FTMO_com are doing this very well. So why spend tons of money on acquisition marketing if your future best trading client would be willing to pay to prove they deserve to trade on your platform? Brokers hate toxic traffic and clients who complain when they lose money due to inexperience. The current retail model brings in many unprepared people, which generates support costs and reputational risk. Prop Firms function as an "institutional screening." Instead of opening the doors to just anyone, the Prop Firm requires the trader to go through drawdown rules, risk management, and consistency. For an legacy brokers, acquiring a prop firm means acquiring a pipeline of talent. They cease to be account sellers and become automated headhunters. Large players, such as Interactive Brokers, and even emerging players, like digital banks in Brazil or new brokers in India, are internalizing the "challenge" model. They are creating their own "funded trader programs". Prop firms that just sell tests will disappear over time. Those that educate their traders and create better (more lucrative) flywheels. And those that build the technology and education are destined to be acquired or integrated by these giants. Platforms like @cTrader (Spotware Systems) and @dx_trade (Devexperts) and @TradeBlackArrow (@nelogica) are already scaling funded trading programs in hybrid structures. We're releasing the Part II of our Prop Trading report soon, that will give you front row seats to this seismic shift in the retail trading landscape.

The latest Rule 605 data (March 2026) reveals a bifurcation in market structure bifurcation most of the industry is not watching. In mapping seven of the U.S. largest equity market makers retail price improvement (PI) and institutional execution quality (E/Q ratio), we see a big difference. Plotted, the results tell a market structure story. Susquehanna sits alone in the upper right. 0.82¢ PI. E/Q of 0.355: Best-in-class on both axes simultaneously. That's not a coincidence, it reflects a routing and internalization architecture that's operating at a different level of optimization than the rest of the field. @Citadel sits in the lower left. 0.58¢ PI. E/Q of 0.635. By far the largest market maker by notional volume ($160B+) but delivering the weakest execution quality in this cohort. Between them: @WeAreHRT, Jane Street, @VirtuFinancial, @xtxmarkets, and @twosigma cluster in the middle, each with distinct tradeoffs between retail and institutional execution quality. What might this mean for the infrastructure on a go-forward basis? 1. Scale does not buy quality. Citadel's volume dominance doesn't translate to execution leadership. Susquehanna runs a fraction of the notional flow, but outperforms on every metric we tracked. 2. The E/Q axis is underweighted in most market structure conversations. Everyone watches PI. Fewer people watch the ratio of executions at or better than the quote midpoint for institutional flow. 3. Rule 605 is obviously a lagging indicator. The March 2026 data reflects February routing decisions. By the time this is published, the firms have already adapted their strategy. Which means the gap you see here is possibly the floor, not the ceiling. The Execution Frontier isn't a ranking, as there is a ton of data around product mix not captured here, but we are watching where this trend pushes U.S. markets and regulation in the near future. We'll be publishing the full analysis at merchantseven.com soon. Stay tuned!

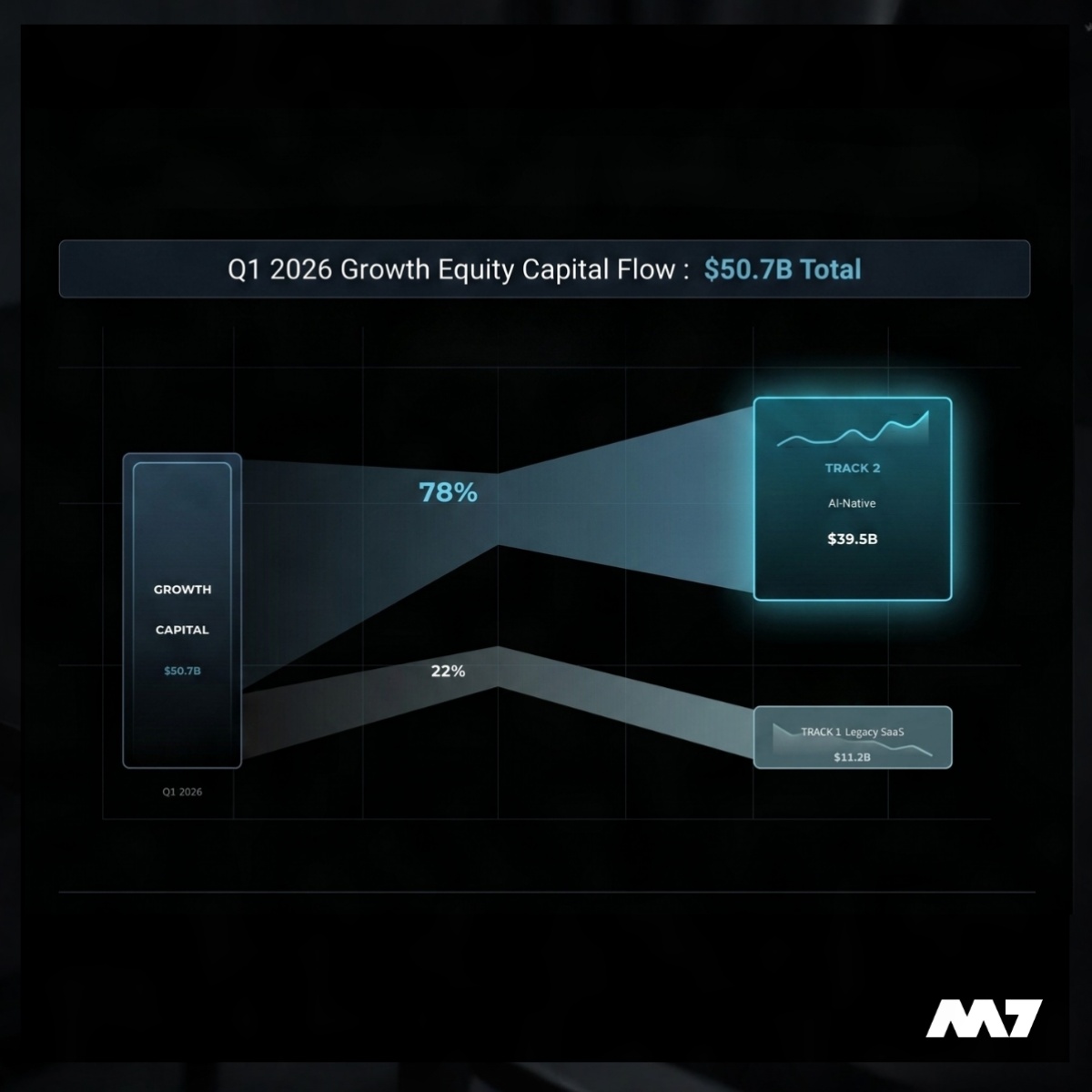

There are two AI tracks right now. Track 1: Adding a chatbot to a legacy SaaS product. Track 2: AI-native capital structures where the model is the business. 78% of Q1 growth equity deals went to Track 2. Serious platform builders know the difference. There has never been a better time to build real technology.

The most important crypto news of the latest days didn't come from a blockchain foundation. It came from @MorganStanley. The launch of the MSNXX government money market fund, designed specifically to hold reserves for stablecoin issuers in compliance with the GENIUS Act, is a watershed moment. It mirrors the post-2008 financial crisis, where money market funds became the de facto safe harbor for institutional capital. We are watching the institutionalization of stablecoin infrastructure in real-time. This marks the beginning of the utility era. The infrastructure layer is maturing rapidly. There has never been a better time to build compliant, next-gen financial systems.

The clearing infrastructure wave is here. In the last 90 days: ↳ @AlpacaHQ - $ 150M Series D, acquired @WealthKernel, entered Europe. API usage up 4x QoQ. ↳ @ClearStreetLLC - new fundraise + IPO planning. $ 649M raised to date. ↳ @DriveWealth - new CEO, hired Fidelity's head of client growth as CRO, Tradeweb's global risk head as CRCO. ↳ GTN - new CEO, Type 1 SFC license secured in Hong Kong. ↳ @apexfintech - AI Suite live. Prediction Markets platform launching Q2 (turnkey FCM, 24/7 clearing, one API). ↳ @RQDClearing - live on @EquiLend. This is not a coincidence. The correspondent clearing model is breaking. The next generation of broker-dealers needs new rails. The capital is moving before the headlines catch up.

The capital flowing into AI infrastructure right now tells a clear story: the next major leap in trading technology won't be about front-end interfaces, but about the compute layer powering them. As we track the cumulative capital raised across the sector (see chart below), it is evident that building real-time, low-latency AI models for financial markets requires specialized infrastructure. Here are 7 AI infrastructure companies actively reshaping how trading tech operates: 1. @CrusoeAI Solving the compute/energy bottleneck. They use surplus and flare gas to power AI data centers, delivering high-density compute for large-scale trading model training at a lower cost. 2. @togethercompute A full-stack AI cloud platform optimized for inference and open-source models. Increasingly used to run risk analytics and trading strategies at scale. 3. @GroqInc Built for real-time execution. Their custom LPU chips deliver ultra-fast inference, making them ideal for live trading signals, HFT, and market simulation. 4. @LambdaAPI A specialized, high-performance GPU cloud purpose-built for AI training. They are serving quant teams and developers by competing directly with hyperscalers on availability and cost. 5. @DatabentoHQ Market data built for the AI era. They provide real-time and historical APIs (equities, futures, options) that are normalized, low-latency, and explicitly designed for quantitative and AI-driven strategies. 6. @SambaNovaAI A full-stack platform with custom silicon. Their architecture handles data-intensive financial AI applications, powering complex trading analytics and risk modeling efficiently. 7. @SiliconFlowAI Focused on low-latency inference and fine-tuning for large models. Their infrastructure supports real-time data feeds and AI trading platforms that cannot afford execution delays. The foundation of the next-generation capital markets is being built right now. Who else should be on this list?

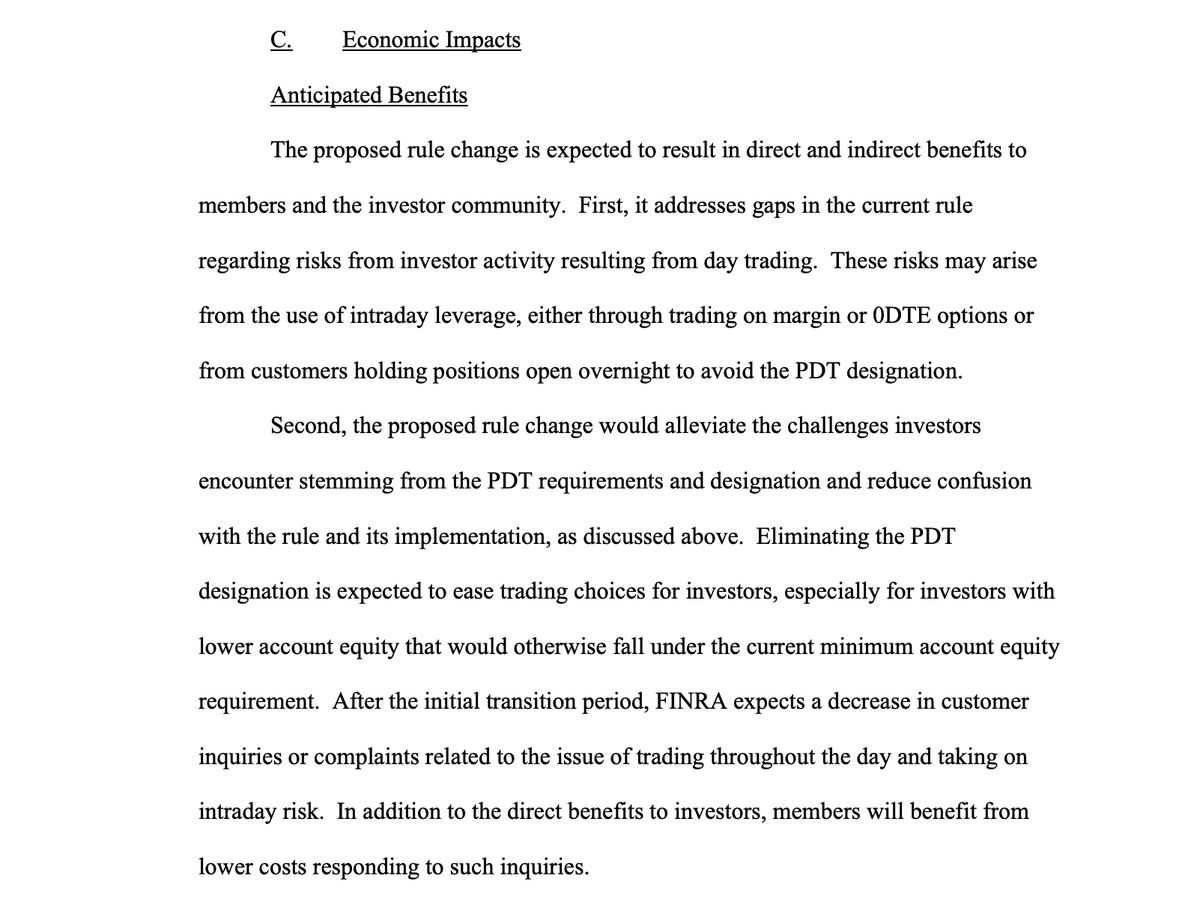

The SEC just removed the Pattern Day Trader (PDT) rule, ending the $25,000 margin requirement for small investors. For retail traders, this is democratization. For retail brokerages, this is an infrastructure stress test. Removing the capital barrier means exponentially higher order flow velocity, increased margin exposure, and a completely different risk profile for clearing systems. The brokerages that win this cycle won't be the ones with the best marketing. They will be the ones whose matching engines systems can handle the new growth of retail participation.

When tracking the institutional adoption of digital assets, it is easy to lose sight of the true scale of the global market. The logarithmic radar chart we made reveals exactly where we stand today in the transition to an onchain economy. The inner ring represents the current market cap of tokenized Real-World Assets (RWAs). The outer ring? The total global market cap of those exact same asset classes in the legacy economy. Here is what the data actually tells us about the current state of the market: 1. Fiat Currencies: A $100 Trillion global footprint, yet only $160 Billion currently runs onchain via stablecoins. 2. Sovereign Debt: A $100 Trillion market, with a mere $11.5 Billion tokenized to date. 3. Equities & Real Estate: Combined, residential real estate and global stocks represent $395 Trillion in traditional wealth. Their onchain penetration today? A near-invisible fraction at $1.5 Billion and $150 Million, respectively. At M7, we don't view the massive void between these two rings as empty space. It represents the largest Total Addressable Market (TAM) expansion in the history of capital markets. The sandbox phase is over. As we have covered over the last few weeks with moves from @EuroclearGroup, @Mastercard, and ICE, legacy infrastructure is no longer fighting decentralized rails; they are actively absorbing them. Traditional finance has recognized that onchain capital efficiency, instant T+0 settlement, and 24/7 liquidity are fundamentally superior to siloed legacy systems. The race is no longer about building the base infrastructure rails. The challenge now is to leverage this new interoperability to capture migrating institutional liquidity, seamlessly merging TradFi and DeFi. As we are saying; Market structure doesn't evolve by arguing with the past. It evolves by building a superior future that makes the old ways simply obsolete. Let’s accelerate outcomes.

The $7.3B Agentic AI Market Just Hit an Inflection Point. But Infrastructure, Not Agents, Will Decide the Winners It’s a market structure shift, exactly like the ones we’ve seen before in finance. Here are 5 historical analogs that show precisely how these transitions play out and who captures the real value. 1. Telegraph → Telephone (1844–1920) Real-time communication replaced mail-based banking. Winners: Western Union, AT&T, and the exchanges. Losers: Post Office and local operators. Outcome: Centralized players that owned the communication layer captured the monopoly value. 2. Stock Ticker → Electronic Trading (1887–2006) Open outcry gave way to computerized matching. Winners: Technology providers and the first HFT firms. Losers: Floor traders and traditional brokerages. Outcome: Speed was the initial edge, until regulation and transparency became the new moat. 3. ATM Networks → Branch Banking (1965–2010) 24/7 self-service replaced branch-dependent models. Winners: Banks that invested in infrastructure. Losers: Traditional teller roles (shifted to sales). Outcome: Branches became cost centers instead of revenue centers. 4. Credit Cards → Checks (1950–2000) Paper clearing moved to electronic networks. Winners: Visa and Mastercard duopoly. Losers: Small retailers forced into the system. Outcome: Interchange fees and network effects locked in structural power. 5. Online Banking → Neobanks (1995–2025) Branch-first models lost to digital-first players. Winners: Tech-native fintechs. Losers: Slow-moving incumbents. Outcome: Brazil’s Pix processed 428 billion transactions in 2023 alone, speed and convenience won. The pattern is always the same: Speed creates the first wave → backlash and friction follow → infrastructure + governance win the long game.

📌 M7 Annual Letter - by Pierce Crosby: piercecrosby.com/f/merchant-sev…

March 2026 will be remembered as the month the "Great Convergence" transitioned from a strategic roadmap to a functional reality. We have long stated that the digital asset tech stack would eventually "eat" traditional finance; this month, we watched it happen in real-time across the world’s most significant balance sheets. At M7, we don’t track prices, we track the migration of infrastructure. Here is the definitive landscape of the new financial architecture. 1. The RWA Power Rankings: Trillions in Transit The quantitative proof of institutional adoption is no longer a debate. Traditional giants and crypto-native pioneers are merging into a single leaderboard. With @HSBC (Orion) crossing $350B in exposure and Figure at $15.79B, RWAs have emerged as a dominant institutional asset class. As companies like @BlackRock ($1.99B) and @OndoFinance ($1.93B) continue to scale, we are seeing the conversion of the world’s safest assets into internet-native settlement rails. 2. @Mastercard and the "B2B Plumbing" Standard Mastercard’s rollout of its "Crypto Partner Program" with 85+ digital asset companies (including @circle and @PayPal) isn't just another partnership, it is a standardization of B2B plumbing. Mastercard is positioning itself as the ultimate translation layer, ensuring blockchain technology plugs directly into enterprise compliance. The front-end feels like TradFi; the backend settles with the instant efficiency of a stablecoin. 3. Complexity Goes On-Chain: @Citi & @EuroclearGroup The narrative that blockchain is only for simple T-bills is dead. Citi’s issuance of a digitally native structured note on Euroclear’s blockchain proves that the "core plumbing" of European finance, which processes €1 quadrillion a year, is now hardwiring digital ledgers into legacy systems. If a product as complex as a structured note can live on-chain, everything can. 4. @Nasdaq & @krakenfx: Breaking the Wall The wall between regulated equities and permissionless DeFi has officially collapsed. Nasdaq’s partnership with Kraken (@Payward) to build the @xStocksFi Gateway allows tokenized equities to move fluidly between permissioned and open networks. This creates a world where a single layer of collateral can margin a portfolio across both TradFi and DeFi venues, radically increasing capital efficiency. 5. The ICE / @okx Boardroom Bridge When the Intercontinental Exchange (ICE), the parent of the @NYSE, takes a seat on the board of OKX, the signal is clear: the future of global capital markets will run on digital infrastructure. This isn't just an investment; it’s the fusion of deep institutional governance with 24/7 high-performance rails. 6. AI Dispersion: Hardware Over Hype In the equity markets, we are witnessing a brutal "creative destruction." While the U.S. market capitalization heads toward $60.4 trillion, hardware-centric winners outperformed software incumbents by a staggering 171% to 72%. The market is no longer rewarding "vibe coding" or software hype; it is rewarding the physical compute and tangible demand required to run the modular world. 7. The Rise of the "Digital Employee" We have moved from experimental bots to production-ready "digital employees." @BNYglobal Mellon’s "Eliza" platform is now facilitating the onboarding of agents designed for settlement prediction and fraud detection. This is the functional realization of our thesis: AI is the "operator" of the new financial rails, reducing costs by 40-60% and enabling the shift from T+1 to atomic T+0 settlement. 8. Institutional Conviction & 24/7 Resilience March proved that institutional commitment is the market’s floor. @BlackRock IBIT recorded $1.32B in net inflows, signaling that global allocators view corrections as structural entry points. Furthermore, as the "Hormuz Shock" sent oil past $120, traditional markets were paralyzed by weekend closures. Meanwhile, on-chain platforms like @HyperliquidX demonstrated the necessity of 24/7 infrastructure for real-time risk management. 9. Strategic M&A: Buying Certainty The pace of acquisitions reveals a "flight to regulation." From @Ripple $1B deal for @GTreasury to ICE’s $2B stake in @Polymarket, the message is consistent: incumbents are buying regulated, battle-tested innovators to bypass the "regulatory landmines" of yesterday. This is being bolstered by the implementation of the CLARITY and GENIUS Acts, providing the federal framework GSIBs need to move full-steam ahead. 10. The Retail Prop Trading Reset This month, M7 officially released Part 1 of our latest research: "The Retail Prop Trading Reset". We are calling the end of the "high-churn casino" era where firms operated like lottery tickets. After the collapse of 100+ firms, we are seeing a "Great Legitimacy Shift" toward B2B2C infrastructure. The prop firm is no longer a standalone destination; it is becoming a feature of the broader brokerage stack where longevity, education, and compliance are the new competitive moats. 11. M7 Vision: Attaining Gravity In our Annual Letter, Founder @crosbyventures noted that M7 has "attained gravity." We have transitioned from a strategic advisory into a self-sustaining engine of financial transformation. In an environment defined by fragmentation, M7 acts as the flashlight in a dark room, helping founders and institutions build for the long term while the "old ways" simply become obsolete. The race is no longer about building the rails, it’s about how fast you can operate on them. Adapt, Create, and Survive. Let’s accelerate outcomes!

📌 Part I of "The Retail Prop Trading Reset" report: merchantseven.com/Research

We just released our State of the Prop Firm Trading Industry. This is a part 1 of 2 series about the inner workings and history of prop firms. If you work in trading tech, you'll want to read this as it represents a seismic shift in new traders entering the market. Get the report below

@Bakkt It's always interesting to see how established companies share their future plans, particularly when it comes to digital assets.

@TheCryptoSquire As digital assets move closer to mainstream financial services, the focus shifts to infrastructure that can handle global scale and regulatory complexities.

The early focus on developer tooling and cultivating a robust ecosystem has created a powerful network effect that's incredibly difficult for new layers to replicate. This strong foundation not only solidifies its current position but also uniquely prepares it for broader institutional adoption as regulatory clarity continues to emerge.

!Kent www.kent.vc @wearekent_

4K Followers 3K Following Making memes while fighting with cancer #NGMI I will spend my last days making memes Building NFT project !Kent @kent_vc_ https://t.co/innEmuM20e

TrendGo Trading Syste... @TrendGo_

675 Followers 143 Following Clarity over chaos. The Trading System that shows you what matters - before it matters. No signals. No hype. Just structure. 👉 https://t.co/rWj8YKS67k

Riley Rosebee @be_rosebee

3K Followers 1K Following

Will @WClemente

795K Followers 3K Following market enjoyer, thinking about them @stix. not investment advice, personal opinions which change, etc.

Patrick Dunuwila, CMT @Pdunuwila

5K Followers 2K Following

stefan springer @gnalsa

192 Followers 2K Following

Millennium Twain #Tru... @MillenniumTwain

2K Followers 7K Following A Million-fold refinement in our EM-Field Mapping of Creation in Electrons, Protons, DiProtons, Alphas, FTL StarShips, Astrospheres, Cluster/Streams, Galaxies —

Ⓜ️𝗶𝗱𝗮�... @MidasBull

535 Followers 7K Following Trading✶Brain✶Biohacking✶Longevity✶Biotech✶Science✶Tech✶AI✶Wellness✶Martial Arts✶Liberty

Hans @HansonBirringer

3K Followers 2K Following

Jacqueline @HintzSigmu12852

200 Followers 7K Following

Dr Helmut @btcWhaleclub

25K Followers 575 Following Apparently CT founder. Class of 2013. Co-Founder @CL0AKL2 Tweets are my own.

Lucas Marin @marintrader_

1K Followers 429 Following US small caps trader that went part time to make @tradeblackarrow the main trading platform in US Instagram: @lucasmarin_ YT: https://t.co/7HNoc3strq

Shawandaa @ShawandaKarn

429 Followers 3K Following Bassist and programmer. Working to help end the homelessness crisis in San Diego.

John Muchow, MSCS @JohnMuchow

54K Followers 2K Following Full-time growth stock/options trader. Creator of TrendPro suite, top-rated @TradingView indicators based on years of collaboration with top performers in USIC.

Dreamy Home Spaces @DecorssStunning

1K Followers 3K Following Beautiful interior design from around the web. Daily updated Amazon product links with over 4.5 ⭐ and 🆙

Kinfo @Kinfo

10K Followers 481 Following kinfo tracks your trading performance, verified through integration to brokers. RD: https://t.co/qAFoFjA1rO

Francis @DeGeneralissimo

10K Followers 590 Following

Rajat Kumar Singh @tradingwick_

15K Followers 30 Following Stocks | Crypto | Prediction Markets Brand & Product Marketing (Fintech) Previously @TradingView All glory to GOD.

Andrey Povazhnyi @w0rse

167 Followers 471 Following Engineering manager @tradingview Built https://t.co/ajLfyOQcY6 AI copilot for TradingView

ParimalPatel @Parimalpatel7

418 Followers 2K Following

Petr Stejskal @SmaRty595

2 Followers 50 Following

Raphael Cordeiro @RCordeiro_Trade

181 Followers 971 Following Community Strategy Lead @ M7 | Fintech Growth Specialist | Crypto Analyst | Trader

matthew 💭 @yo_itsmatt

16K Followers 2K Following head of product marketing @solanafndn // prev @okx @wallet @cryptocom @mit // like or @ ≠ endorsement // no wahala or financial advice

📊 JHill 🦇🔊 @JohnnyCrypto3

3K Followers 5K Following Cryptocurrency Trader co’17 | SAG-AFTRA - Stuntman | NFT Photographer | Audiophile | Professional Rollerskater

CJ @cjxotrade

2K Followers 5K Following No crying in the casino. Global financial markets, investing and trading at Mandelbrot

Paweł Łaskarzewski @PawelSynapse

118K Followers 3K Following Micro, Macro, Crypto Economy @NomadFulcrum | DeFi is the ultimate revolutionary act | I am DeGen - DEcentralised GENeration | The future is liquid

Milana @Milana19593153

3 Followers 3 Following

Scheplick @scheplick

18K Followers 1K Following I watch markets, create content about them, and build top trading & investing tech with @merchantseven

Jonathan H. Wage @jwage

8K Followers 596 Following Founder @TradersPostInc. I like to build stuff. Trading automation software is my thing. Open-Source software PHP @doctrineproject @symfony.

Hải @btc_apprentice

103 Followers 1K Following I'm here to learn about #blockchain adoption & $crypto trading

🛡️Zac @zacxbtc

9K Followers 8K Following | PHILANTHROPIST | INVESTING | IDEATION | NFA| POW@ 300Films @20thCentury 60Shows @ABC @FOX @DisneyStudios | $4B Production/ Marketing/Distribution & Growth

Skye @_SkyeLiu_

18 Followers 12 Following Director Partner Operations @merchantseven #Web3 #Metaverse #DeSoc #

Stan Vick @stan_vick

316 Followers 370 Following Founder & CEO at @11thestate | $250M+ claimed for investors by binding fin, legal & AI tech together

Lucas Marin @marintrader_

1K Followers 429 Following US small caps trader that went part time to make @tradeblackarrow the main trading platform in US Instagram: @lucasmarin_ YT: https://t.co/7HNoc3strq

BlackArrow Trading @TradeBlackArrow

105 Followers 30 Following Your edge in futures & equities. Charts, execution, and analytics. Built for traders who are serious about performance.

John Muchow, MSCS @JohnMuchow

54K Followers 2K Following Full-time growth stock/options trader. Creator of TrendPro suite, top-rated @TradingView indicators based on years of collaboration with top performers in USIC.

Francis @DeGeneralissimo

10K Followers 590 Following

Kinfo @Kinfo

10K Followers 481 Following kinfo tracks your trading performance, verified through integration to brokers. RD: https://t.co/qAFoFjA1rO

Raphael Cordeiro @RCordeiro_Trade

181 Followers 971 Following Community Strategy Lead @ M7 | Fintech Growth Specialist | Crypto Analyst | Trader

Pierce Crosby @crosbyventures

9K Followers 6K Following Building @merchantseven, ex @tradingview, @theblock__ @refintiv @stocktwits

Scheplick @scheplick

18K Followers 1K Following I watch markets, create content about them, and build top trading & investing tech with @merchantseven

Milana @Milana19593153

3 Followers 3 FollowingYou might like