MayRetire @MayRetire

Joined October 2024-

Tweets146

-

Followers188

-

Following30

-

Likes144

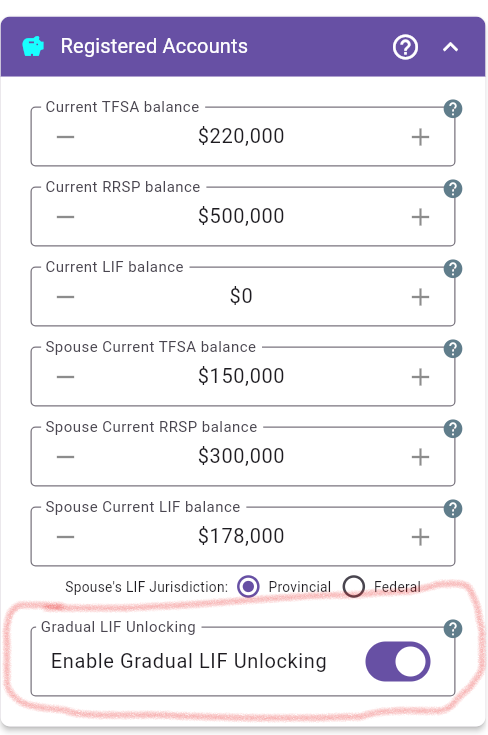

New MayRetire feature: Gradual LIF Unlocking This feature was suggested by one of MayRetire’s expert users. MayRetire now supports Gradual LIF Unlocking. When enabled, it can model the tax-deferred transfer of unused annual LIF maximum withdrawal room into an RRSP/RRIF, where this strategy is supported by the LIF jurisdiction. This can be especially useful for plans with locked-in retirement funds, because it may affect future flexibility, withdrawal planning, and long-term tax projections. If you have a LIF/LIRA in your plan, it may be worth checking whether this new option changes your retirement projection.

Another MayRetire Zoom presentation by @67Dodge on June 11 7pm. Registration link: us06web.zoom.us/.../register/l…

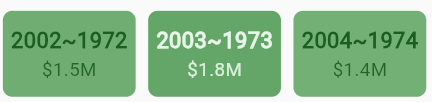

MayRetire Backtesting Update Based on user feedback, I’ve updated how historical backtesting works. Previously, if a retirement plan extended beyond the available historical return sequence, MayRetire filled the remaining years using deterministic projection assumptions. That could make some backtest periods less purely historical. Now, backtesting uses only the historical return sequence. If a plan runs past the latest historical year, the sequence wraps back to the first historical year, so every starting year gets a full-length test without mixing in projected returns. You may now see wrapped periods labeled with ~, for example: 2003~1973. That means the sequence starts in 2003, reaches the end of the historical data, then continues from the beginning of the historical sequence through 1973. If you’ve used MayRetire backtesting before, it may be worth running your plan again to see whether this change affects your historical backtest results Thanks to the users who pointed this out and helped make the backtest results clearer and more consistent

MayRetire now has initial support for Whole Life Insurance and similar permanent policies with fixed premiums and predictable death benefits. You can enter an existing policy or test how adding a new policy might affect your retirement plan. The model is intentionally simplified: annual premium, payment duration, current death benefit, and optional benefit growth. That is enough to capture many of the insurance effects that matter in retirement planning, including premium cash flow, survivor support, and estate impact. This can be especially useful for couple plans, where insurance may change survivor security and final estate outcomes. Try it to see how insurance affects: - survivor planning - estate value - premium cash-flow needs debt or collateral-loan scenarios, if applicable Use actual policy details where possible and review assumptions carefully.

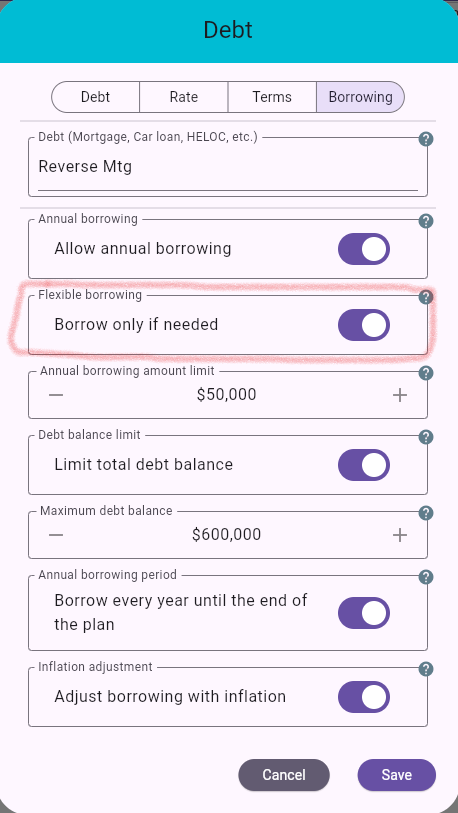

New in MayRetire: Borrow only when needed You can now model debt as a retirement safety net instead of a planned annual draw. With the new Borrow only when needed option, MayRetire will only use borrowing if other funding sources are not enough to support your required income. If the plan never needs the extra cash, no borrowing happens. This can help test resilience against difficult scenarios like poor sequence of returns, expensive late-life care, or other unexpected cash needs. It can also help model backstop strategies such as a HELOC, reverse-mortgage-style borrowing, or borrowing against permanent life insurance. Set an annual borrowing limit, optional maximum debt balance, and see exactly when borrowing is triggered, how much is used, and how it affects income, debt balance, and final estate.

MayRetire video intro by @67Dodge youtube.com/watch?v=viLuB6…

MayRetire now supports principal residence planning. You can include your home directly in a retirement plan and test different paths: * keep it to the end and include it in the estate * sell it later and use the proceeds * downsize and account for either extra cash or a shortfall This can make a huge difference when looking at long-term estate value, especially for households where the home is one of the biggest assets. We also enhanced debt planning so it can handle reverse-mortgage-style scenarios. That opens up some interesting “what if things get tight?” planning: instead of assuming the only options are sell investments or fail the plan, you can test whether borrowing against home equity could provide a safety buffer in more challenging cases

MayRetire can now model debts that start later in retirement, not only debts that already exist today. You can set the year the debt begins, the initial borrowing amount, interest rate, and repayment style. Future debt balances are included in projections, charts, estate calculations. Compare Plans now lets you compare debt balances and annual debt payments across scenarios.

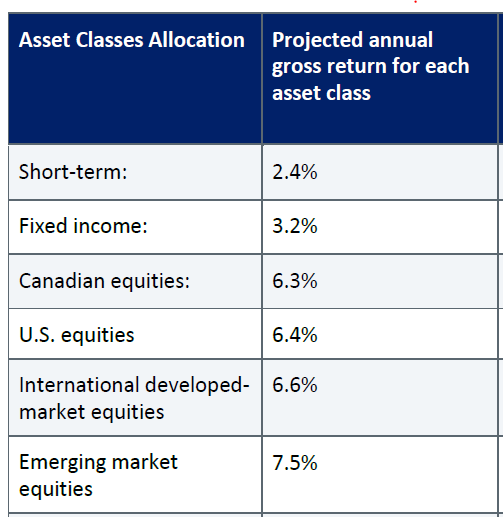

MayRetire has been updated with the FP Canada 2026 Projection Assumption Guidelines. Inflation stays at 2.1%, but most equity return assumptions were adjusted slightly lower. We also updated volatility and asset correlation assumptions used in simulations. Run your plan again with the new FP Canada guideline assumptions and see what changed. Reminder: MayRetire’s Investment Portfolios feature lets you set custom rates of return for each portfolio if your own assumptions differ

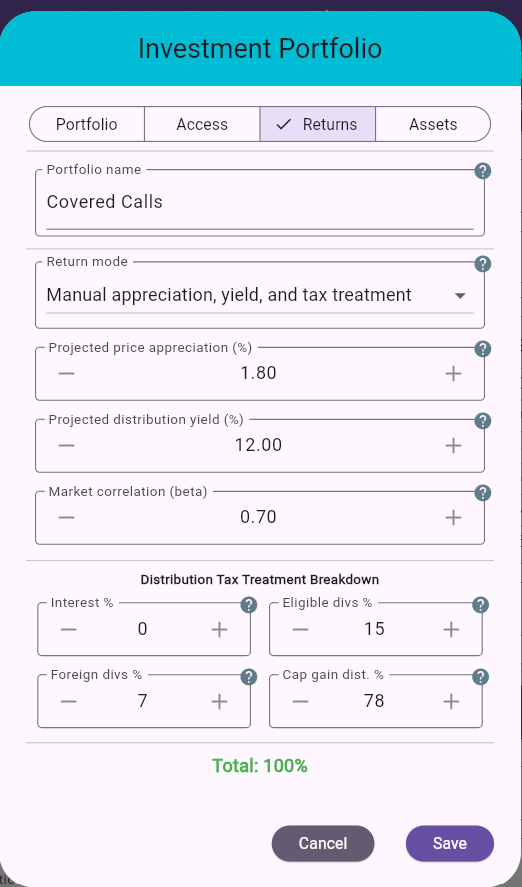

New in MayRetire: Investment Portfolios A major new feature, shaped heavily by user requests. You can now model separate taxable portfolios alongside the regular non-registered account, each with its own ownership share, asset allocation, capital-access rules, distribution policy, and return assumptions. This makes it possible to: - Split taxable assets into portfolios with different ownership shares or asset allocations. - Model an income-focused portfolio where distributions are prioritized for withdrawal before other optional income sources, while capital can remain protected until needed. - Set aside part of taxable capital for a specific purpose, while leaving other capital available for normal retirement spending. - Plan when a separate taxable portfolio should become available for spending or be sold and merged into the regular non-registered account. - Use FP Canada asset-class assumptions for each portfolio when those categories are enough. - Customize an income portfolio with separate price appreciation, distribution yield, tax-treatment mix, and market behavior through a reference allocation and correlation (Beta). Try it now if this matches something you have been trying to model. To learn more about Investment Portfolios, visit: mayretire.com/resources/tuto… As always with a new major feature, there may be rough edges, so feedback and suggestions are very welcome. MayRetire is becoming a truly community-driven planning tool!

We have just rolled out the Annual Cash Flow Chart. While this new chart doesn't expose any new data that wasn't already in your plan, it visualizes your annual numbers in a much more expressive and intuitive way: MayRetire maps your annual, inflation-adjusted data to show you exactly where your money comes from and where it goes. It makes understanding the balance between your income, your taxes, and your spending easier than ever. We also understand that a growing number of charts can sometimes feel overwhelming, and not every visual is useful for every user. That is why MayRetire allows you to easily hide any chart—so you can declutter your view and focus only on the metrics that matter most to you.

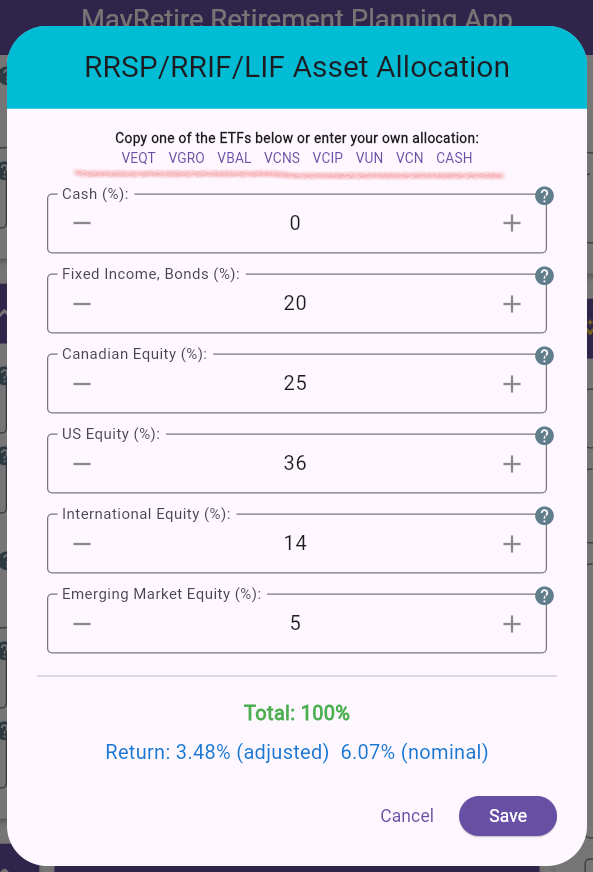

All are conveniently available for quick asset allocation selection @MayRetire

Portfolio returns for the Vanguard suite of asset allocation ETFs, available at 5 risk levels. To the end of March 2026.

We heard requests for more visibility into how MayRetire calculates taxes, so we added a new Annual Tax Report. This new report gives a year-by-year view of taxable income, deductions, federal and provincial tax credits, surtax and health premium where applicable, and total tax payable. It’s designed to make the tax side of the plan easier to review and easier to trust. You can switch between Detailed and Compact views, and also view amounts in either Today's dollars or Future dollars.

A look at a retirement cash flow review using @MayRetire You can also sign up for a how-to-use MayRetire Zoom call this Thursday. 12 pm EST or 7 pm EST. The links are in the post. cutthecrapinvesting.com/2026/04/05/glo…

MayRetire now supports debt planning for mortgages, HELOCs, and loans. This first step brings debt payments into retirement cash flow, taxes, estate impact, and detailed projections, making it easier to see how debt changes the full retirement picture.

Dale Roberts from Cut the Crap Investing (@67Dodge) is hosting a Zoom meeting on April 16th to walk through MayRetire's features and demonstrate how to optimize a retirement plan using the software. You can join a 12 pm or 7 pm EST session this Thursday, April 16th. Time: Apr 16, 2026 12:00 PM Eastern Time Join Zoom Meeting: us06web.zoom.us/j/86501370741... Enter this Passcode: 156627 Meeting ID: 865 0137 0741 Time: Apr 16, 2026 07:00 PM Eastern Time Join Zoom Meeting: us06web.zoom.us/j/88085678747... Enter this Passcode: 828943 Meeting ID: 585 884 9710

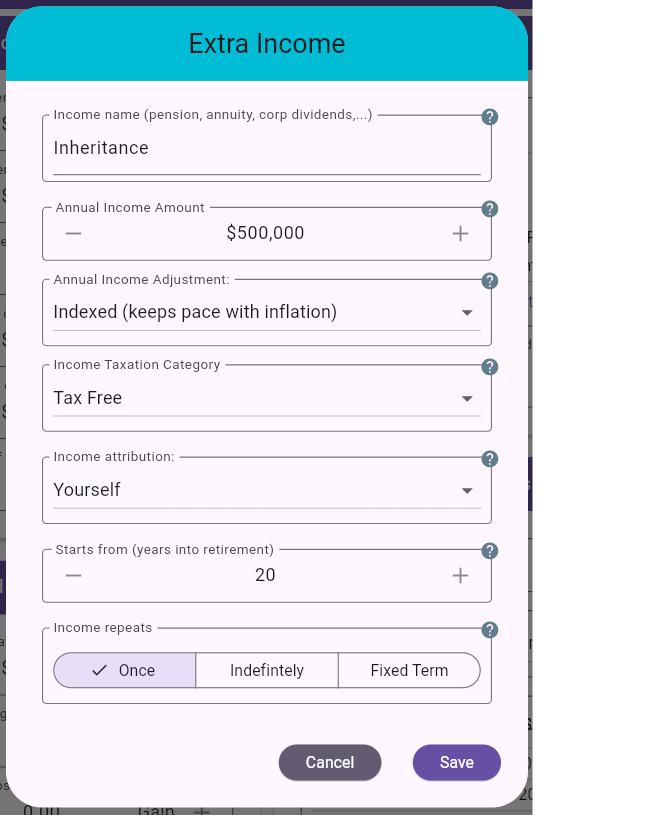

💡 Quick Tip for MayRetire Users: Wondering how to model a home sale, downsizing, or an inheritance? You don't need a complicated workaround. Just add it as 'Extra Income', set it to 'Tax Free', and click 'Once' at the bottom. Check out the screenshot below to see exactly how to set it up!

MayRetire now supports charitable donation planning, one of the most requested features from our users. You can now model: * after-tax cash donations * in-kind donations from non-registered investments * corporate in-kind donations This first iteration helps make charitable giving part of a more tax-efficient retirement plan, with donation amounts and related tax credits reflected in results, charts, tables, and PDF reports. This is just the beginning. We plan to keep improving donation support as MayRetire evolves based on user feedback.

Dale Roberts from @67Dodge took a recent Globe and Mail 'Financial Facelift' case—featuring DB pensions, variable spending, and a $1.3M inheritance—and ran the numbers through MayRetire. It is a great read on how to stress-test your cash flow while awaiting an inheritance. Check out his full breakdown and see how the plan holds up: cutthecrapinvesting.com/2026/04/05/glo…

New post. I look at a Globe & Mail retirement review scenario and run a retirement cash flow plan at @MayRetire I started playing around with the numbers, next thing I know it turned into a post ... cutthecrapinvesting.com/2026/04/05/glo…

Brian McReynolds @BrianMcR27

15 Followers 40 Following

Michael John @spennyspeaks

142 Followers 557 Following Sales and marketing guy, and humble student of all things investing

Francis Cahill @frcahill

35 Followers 408 Following

NL @Hab_Stanley1993

3 Followers 105 Following

WHM @wmcleod2

3 Followers 182 Following

David Griffith @DWG11

34 Followers 360 Following

l b @lb4652332031531

41 Followers 772 Following

GK @Graeme5464

45 Followers 2K Following

Cliff Jamieson @jamieson_c

40 Followers 778 Following

Brandon Chau @bchau89

7 Followers 3K Following

Mat Drouin @matdrewin

774 Followers 993 Following I build things. Claudemaxxer. Currently building @diptrackapp

Robert Cookson @rcookson

56 Followers 368 Following

FreemansPotpourri @MFreema27599163

123 Followers 2K Following For entering contests, and the occasional witty comment. #SFB12 #MurakamiFlowers. Cowtippers on Upland and Yahoo DFS. 49ers, Raps, Jays, Ducks, Wolverines.🇨🇦

Mar @Mar15151440

0 Followers 820 Following

Roka @Roka55227041192

48 Followers 192 Following

Dave Cee @DeeCee_09

589 Followers 341 Following 🇨🇦 Military Police Veteran, full time Investor, part time Day Trader, current provincial Investigator

Gord @gordpenner

68 Followers 515 Following

Аdministrator @net25366

23 Followers 379 Following

Russ @RussBarden

156 Followers 801 Following Sports fan, father of 2 kickass kids, heavy equipment operator, home renoer

Investing Can @investingcan

320 Followers 2K Following 🍁 canada 🇨🇦|| investing || family 🏠, food 🥘, outdoors 🌲 || product manager || generation x

Robert West @westof3000

99 Followers 836 Following

Canuck Dividends| �... @HubbyWifeshubby

1K Followers 690 Following Dividend investor / Shakepay Club 365 member - cdnrascal / IG - Canuck Dividends / animal rescue supporter /passive income 🖥 👨💻 📊 📈

Kathleen Hunt @Kathlee23137956

82 Followers 2K Following

Karin @Karin1227191

16 Followers 316 Following

Red Panda @japbeet

13 Followers 65 Following

Rocky @Rocky46215911

98 Followers 564 Following Father, hockey fan, energy enthusiast and libertarian

Gianluca Ianiro @GianlucaTORONTO

83 Followers 646 Following 🇨🇦🇮🇹Husband | Father | JUVE ⚽️ Supporter| Engineer | Tech Lover | Bullish on BTC and ETH | Enabling Digitial Transformation |Freelance Website Developer |

Duane Rieger @riegd888

1 Followers 746 Following

Evan Jay @EvanHernder

482 Followers 169 Following Providing financial literacy coaching for Canadian solopreneurs. Gain confidence and start to Live Wealthier.

Wkg @Wkg1341611

7 Followers 56 Following

Craig Wilson @craigdubya

300 Followers 5K Following McD’s crew OG, Behavioural Science geek. Likes, follows and RT's are not endorsements/investment advice/views of firm

earlerose @EARLEROSE

24 Followers 5K Following

karen @karen97144603

11 Followers 132 Following

HIM is my day job @Turboo_30

275 Followers 463 Following Statistics & Facts are Verified Truth. Don't let others (truth) muddy the water. Intelligent debate is healthy. Small Town Farm Families are our Bedrock.

Anthony Michael Demar... @tonydemarin

219 Followers 4K Following

Shaheen @sha_za_ha

34 Followers 316 Following

Chris Blender @ChrisBlender

2K Followers 2K Following Always bet on yourself. Former EY Entrepreneur Of The Year finalist. Transplant recipient. Frustrated golfer

Stephen Haley @SchaleyRo

23 Followers 108 Following

Caroline @c_tdot

74 Followers 746 Following

Debra Carswell @debkoz

20 Followers 350 Following

Renu Khosla (she/her) @RenuatEAP

259 Followers 738 Following EAP Specialist, Mediator, and Well Being Advocate. Views are my own.

Brenden Myers @brebden

177 Followers 2K Following

Globe Advisor @GlobeAdvisor

1K Followers 235 Following Globe Advisor brings you expert financial tools, in-depth analysis and advice to help you grow your clients’ portfolios

TaxTips.ca @TaxTipsCdn

5K Followers 170 Following Canadian tax, financial and investing info, tax and other calculators, tables of tax rates/tax credits. Goal: to be THE free reference site for Canadian tax.

TIER Wealth @TIERWealth

353 Followers 68 Following TIER Wealth is built on a foundation of trust, deep relationships, and a commitment to always putting our clients first. Tax | Investment | Estate | Retirement

Martin Pelletier @MPelletierCIO

73K Followers 4K Following PM @TriVest_WAPC | Columnist @fpinvesting | Pre-order NEW BOOK: https://t.co/3ELQLqsGvg

Drew Feldman, APMA® @TheDrewFeldman

2K Followers 480 Following • Flat-fee financial planner to film, TV, and theater pros turning career breakthroughs into financial stability • Author, Money for Makers • Check it out ↓

My Own Advisor @myownadvisor

13K Followers 4K Following Early retiree thanks to DIY investing in stocks and ETFs. Golf Sicko. Follow with thousands at: https://t.co/fKNE2MnIYP

Rob Carrick @rcarrick

63K Followers 1K Following Personal Finance Columnist for The Globe and Mail https://t.co/IBR6XAaC5u

Call me Sully 🇨�... @paul__sullivan

610 Followers 573 Following Retired business leader. Mentor, advisor & occasional executive coach. Volunteer with World Central Kitchen.

Jonathan Chevreau @JonChevreau

61K Followers 19K Following CFO Financial Independence Hub; author Findependence Day, Columnist at @MoneySense. Semi-retired. @[email protected]. Also on Threads & Bluesky.

CutTheCrapInvesting @67Dodge

10K Followers 4K Following World's best Dad. Husband still in training. Chief Retirement Officer at Retirement Club. Chief Disruptor and investment coach @ Cut The Crap Investing blog

Armchair Financial @ArmchairFinCda

139 Followers 424 Following Sensible information on economics, personal finance and investing.

Brent Schmidt @strategicfuel

144 Followers 329 Following Seeking biz/product owners who want to use #jtbd to ID unmet customer needs. That's what I do.

Benjamin Felix @benjaminfelix

28K Followers 245 Following Helping Canadians make better financial decisions. Chief Investment Officer, Portfolio Manager @PWLCapital; co-host @RationalRemind. Meet with PWL ⬇️

Rational Reminder Pod... @RationalRemind

7K Followers 117 Following Official twitter account for the Rational Reminder Podcast. Hosted by @CameronPassmore and @Benjaminwfelix from @pwlcapital

PWL Capital @PWLCapital

4K Followers 439 Following Investment management & financial planning firm for affluent Canadian individuals, families, & professionals; expert wealth management. Member: CIRO & OCRI

Braden Warwick PhD @WarwickBraden

1K Followers 85 Following Architect of Financial Planning @PWLCapital

Aaron Hector, R.F.P.,... @AaronHectorCFP

8K Followers 433 Following Passion for personal finance, innovative ideas & the well being of my clients. Founder of TIER Wealth in Calgary. President of the IAFP.

Mark McGrath @MarkMcGrathCFP

22K Followers 2K Following I help Canadian physicians treat financial uncertainty. CFP®. DM's are always open. New book out now - grab a copy below ⬇️

Aravind Sithamparapil... @AravindSitham

4K Followers 877 Following Financial Planner at Ironwood Wealth Management https://t.co/j1D9ptbQR0 Tweets are not advice. He/Him

Canadian Dividend Inv... @CDInewsletter

22K Followers 555 Following I invest in conservative, old-school companies that gush free cash flow and pay increasing dividends. It's boring, but it works. Not investment advice.

Devoted Dividend Inve... @DevotedDividend

74K Followers 159 Following 33 | Girl Dad 👶 | Self Made Multi-Millionaire | ❌NFA❌ Learn How I Went From $0 - $9,900 Per Month https://t.co/PXGbkWwzCM

FP Collective @FP_Collective_

2K Followers 34 Following We aggregate content from top Canadian financial planning creators, keeping you informed effortlessly.

Loonie Doctor @LoonieDoctor

2K Followers 94 Following A Canadian physician blogger helping Canadian physicians and other high income professionals improve their financial health while not boring them to death.

Lazy Canadian Investo... @JimChuong

36K Followers 2 Following Turned $300 into a multimillion dollar retirement at age 40. Education. Not advice. Canadian investor in U.S. real estate and U.S. stocks. Discover how:

Barry Schwartz @BarrySchwartzBW

38K Followers 352 Following President & CIO at Baskin Wealth Management. Baskin Wealth or I may own stock mentioned in tweets. None of this is advice - do your own work!

Loonies & Sense @LooniesAndSense

2K Followers 427 Following Lifecycle financial planning and management app for Canadian households 🇨🇦

Boris Rozinov @borisrozinov

202 Followers 643 Following -fno-warn-unticked-promoted-constructors -X Gen

The Globe and Mail @globeandmail

1.9M Followers 1K Following Canada's national news organization. Customer care: @GlobeHelp. Share info with us anonymously: https://t.co/ROPEUBZwoOTrends for United States

You might like