Luis @LuisValue

Microcap investor from Spain. Joined August 2018-

Tweets714

-

Followers161

-

Following1K

-

Likes676

@TheBigBerbowski 30 minutes into the call and they haven't addressed it yet...

@realroseceline I don’t. But I found that article very interesting. It is important how bears think. Time will tell who is right.

Thoughts on $SOFI Regardless of how you dress it up, $SOFI is a lending business at its core. No matter how you package it, they make money by issuing loans and earning the spread, which ties everything to credit quality, interest rates, and funding costs. That’s not just a detail, thats literally the business. The issue is that lending businesses are cyclical, whether people want to admit it or not. When the cycle turns even a little, defaults rise, charge offs increase, and margins compress. It doesn’t take a crisis, just a shift in conditions for things to tighten. This is not a durable model that compounds smoothly, it is a conditional model that works best when the environment is supportive. The risk is also more concentrated than most people realize, which makes it even more fragile. A large portion of the book is in personal loans, which are unsecured and highly sensitive to unemployment and consumer stress. That’s where the first place cracks show up in any downturn. So it’s not just credit risk, it’s concentrated exposure to the weakest part of the credit system. The growth looks great on the surface, and that’s exactly why it’s seductive and pulls people in. But in lending, growth can actually hide risk rather than eliminate it. The real question is not how fast originations are growing, but whether the loans being made are improving in quality or simply increasing in volume. Those two paths look identical in the short term, but lead to very different outcomes over time. Another things I see people miss is how these books are accounted for in practice. A lot of what you see is effectively marked to model, not fully marked to reality yet, because losses are estimated before they are realized. That allows earnings to appear smooth and controlled while risk builds underneath the surface. When the cycle turns, provisions rise and charge offs hit, and what looked stable changes very quickly. This is where the structure of the model really matters, because lending does not scale in a straight line. In good times you see steady growth, low defaults, and stable spreads, which creates the illusion of consistency. In weak conditions, defaults jump, funding tightens, growth slows, and margins compress. The downside tends to accelerate faster than the upside, which is what makes the model fragile. At the same time, $SOFI is trying to position itself as something much broader than a lender. It’s a bank, fintech platform, technology provider, and a financial super app all in one. That sounds compelling, but in practice it makes the business harder to value, harder to execute, and harder to dominate in any one category. It becomes a bit of everything, but not clearly the best at anything. The super app idea also sounds better in theory than in reality. Financial products tend to have low engagement, low loyalty, and are highly substitutable for most users. People don’t build daily habits around their lending apps the same way they do with social, simply out $SOFI is no Instagram. Funding is another critical piece thats underestimated. Even with a bank charter, the model still depends on cost of deposits, securitization markets, and access to capital. If someone else can fund more cheaply, they can price more aggressively and take share. That means the real product is not the app or the interface, it is the cost of capital behind it. Management will always emphasize member growth, product expansion, and engagement metrics. Those are important, but they are not the core driver of value in a lending business. The real driver is risk adjusted returns on the loans being originated. Those two things can diverge for a long time, which is why the story can look strongest right before it starts to weaken. 1/2 👇

@aktieblogg Which broker do you use to invest in these stocks?

@leevalueroach Did they sell an airline recently?

There has been lots of talk about the current situation in Venezuela and what it could mean for global oil markets, so I just wanted to provide some nuance on this 🇻🇪 ⤵️ When people say “Venezuela has the world’s largest oil reserves,” as you undoubtedly have seen being thrown around a lot on here, they are technically referring to a specific accounting definition, not to a stock of easy, cheap barrels ready to flood the market. To unpack that, you need to get into what those reserves are, how they behave in the subsurface, what it costs to turn them into marketable liquids, and how price, technology, and above-ground risk interact. That's a lot to cover, but let’s give it my best shot. On paper, Venezuela has roughly 300–303 billion barrels of proved reserves, about 17 % of the global total and slightly more than Saudi Arabia. The critical detail is that around three quarters of that booked volume is extra-heavy crude from the Orinoco Belt in eastern Venezuela. These are bitumen-like oils with API gravity typically in the 8–14° range, extremely viscous at reservoir conditions and with high sulfur and metals content. So the statement “largest reserves” is really “largest booked volumes of very challenging heavy and extra-heavy oil.” Technically recoverable versus economically recoverable is the first big distinction. The USGS has long estimated that the Orinoco Belt contains on the order of 900–1,400 billion barrels of heavy crude in place, with perhaps 380–650 billion barrels technically recoverable using existing technology. Venezuela and OPEC only book a subset of that as “proved,” but even those proved numbers are sensitive to the assumed oil price and development concept. When prices were strong in the 2005–2014 window, a large portion of Orinoco volumes became economic on paper and were reclassified as proved, driving the headline reserves from ~80 to ~300 billion barrels. Geology and fluid properties are the second big differentiator. Orinoco crudes are extra-heavy, with densities up around 934–1,050 kg/m³, high asphaltene content and sulfur on the order of 3–4 wt% or more, depending on the block. This is a completely different animal from a 33–40° API, low-sulfur Arab Light-style crude. In plain English, that means it's much harder to handle at various stages and each step adds capex, opex and energy use. In other words, the “barrel in the ground” in Venezuela is inherently worth less and depends on a narrower set of buyers. Surface systems and institutional capacity are another constraint. Before the 2000s, PDVSA had a reputation as a technically capable NOC. Since then, you have had a combination of mass layoffs and politicization, under-investment, sanctions, corruption and brain drain. The result is decayed gathering systems, chronic power shortages, refinery fires and upgrader downtime. Finally, integration with global refining and logistics matters for strategic value. Venezuela’s crude slate is optimized for complex “coking” refineries in the US Gulf Coast, parts of Asia and a few European plants. That's a story for another time though, because the length of this analysis is getting out of hand. So when you hear that Venezuela has “the world’s largest oil reserves,” the technically accurate part is that the country has extremely large volumes of extra-heavy oil in place, and a big subset of that was once judged economically recoverable at high price assumptions and booked as proved. The more relevant questions for energy strategy are how many of those barrels are genuinely economic under realistic long-term prices, how quickly they can be brought onstream given infrastructure and institutional constraints, what netback they deliver at the refinery gate, and how exposed they are to being left in the ground if demand peaks. On those metrics, Venezuelan barrels sit much further out on the cost and risk curve than the headline “largest reserves” soundbite suggests. I hope this provided some good context.

One final note on Shift4 $FOUR before I move on to the next company. I recently saw someone claim that Shift4’s acquisition playbook has been “1 + 1 = 3.” That was the entire argument, no evidence, just assertion. Others have echoed that the company’s organic growth potential is “obvious,” again without quantification. Having feelings about a stock is not the same as having conviction in one. As discussed in this analysis, there are material questions around how Shift4 funds growth and what portion of that growth is truly organic, and the cash flow statement shows that the current playbook still relies on external funding rather than internally compounding cash flows. A few readers understood the key takeaway: this is a high-risk, high-reward situation, not a “no-brainer” compounder. Asymmetric bets are acceptable when you recognize them as such, but you should be honest about the difference between a probabilistic trade and a long-term hold. If you plan to hold Shift4 as a true compounder, you should be demanding clear answers to these questions: is organic growth measurable, sustainable, and self-funded? Are acquisitions integrating and creating durable unit economics? Until those answers are visible in the financials, not just in management presentations, you are much closer to speculating than investing. None of this means the bull case is impossible, only that the burden sits with longs to demonstrate, over time and with disclosure, that the growth they are underwriting is both genuinely organic and self-funded rather than engineered through accounting and external capital. Any disciplined investor should be able to map several future outcomes, attach probabilities to each, and adjust those probabilities as new information comes in. When the core questions about cohort paybacks, true organic volume growth, and dependence on capital markets cannot be answered from the statements, the position belongs in Charlie Munger’s “too hard” pile rather than in a high-conviction long or short book. In that sense, the most honest stance here is often not “short” or “all in,” but “not interested for now,” and moving on to situations where the burden of proof has already been met. Thank you for reading this series; whether you agree or disagree with the conclusions, the hope is that it pushed you to think more critically about the company and your own thesis.

“We have three baskets for investing: yes, no, and too hard to understand.” — Charlie Munger Which basket does $FOUR belong in? Shift4: Valuation and Personal Opinion: open.substack.com/pub/bearstone2…

New idea $GPN I want to share a new idea I have been spending time on, $GPN. What draws me to it is how simple the idea is and doesn’t require being genius to understand. You do not need to predict the future or invent a new narrative. The economics are simple and visible if you slow down and look. At its core, $GPN is a payments company that consists of 2 businesses. The first is issuing. Issuing is where cards are created for consumers. Debit cards, credit cards, prepaid cards, etc. They earn fees when those cards are used, but the economics are not attractive. Margins are thin, competition is relentless, pricing power is limited so the returns on capital are weak. The second is acquiring. Acquiring is the merchant side of payments. This is where businesses accept cards, process transactions, manage fraud, settle funds, and integrate software into their operations. Volumes grow over time as the merchant grows. Importantly, the processor does not need to double its cost base to earn that growth.This is the good business with attractive economics, returns on capital, etc. What makes $GPN interesting today is that management is no longer trying to be everything at once. They are selling the issuing business in Q1 26, and returning the cash to shareholders. They are removing bad economics and shrinking the company on purpose. At the same time, they are going all in on acquiring. They recently completed a large acquisition that management expects will increase free cash flow by roughly 50%. They also owned a payroll business. They sold it and returned the cash to shareholders. Just as important, the balance sheet is being brought under control faster than promised. Management has been very clear that leverage will be below 3x by the end of this year, and they are currently ahead of schedule. Debt is coming down as free cash flow rises, not the other way around. This matters because it removes a common overhang and gives the company flexibility to keep returning capital without stressing the business. The management team has shown that they are shareholder friendly and serious about returning capital. They are not hoarding cash. They are not chasing size for the sake of it. Excess capital is being returned back to shareholders through asset sales, buybacks, and a commitment to simple disciplined capital allocation. This is what good capital allocation looks like. Most management teams see cash and feel the urge to build something new. $GPN is doing the opposite. They are subtracting complexity, focusing on higher quality cash flows, and letting the math do the work over time. The reason this matters now is that the company reflected in today’s financials is not the company that will exist in two years. The mix is changing quickly, but the valuation is extremely cheap. Markets are slow to reprice simplification stories because there is nothing exciting to sell. Management expects that in roughly two years, the business will be generating around $5 billion in unlevered free cash flow. The entire company today is valued at approximately $19 billion!! You do not need to be a genius with heroic assumptions to see the disconnect. This is not risk free, the only thing free in life is cheese in a mouse trap. Payments is competitive and there is execution risk, etc etc... But the margin of safety here does not come from perfection. It comes from focusing the business on the best economics while buying it at a price that already assumes very little goes right. If management executes and the cash flow shows up, the valuation will eventually follow. You do not need to predict the future. You just need to wait while the business becomes simpler and more obvious. Management has been buying millions of dollars of stock in the open market. I don’t think you’re getting a 10 bagger here, but a reasonable return is likely with limited risk and a large margin of safety. 🌹

$CRMD has transformed from a cash-burning biotech into a profitable specialty pharma built around DefenCath and the Melinta anti-infective portfolio it's trading at 5x p/e and 9.3x EV/EBITDA, Main risk is probably market skepticism about - DefenCath’s durability, - Melinta underperforms - post-TDAPA reimbursement margin pressure, - more cash burn + dilution

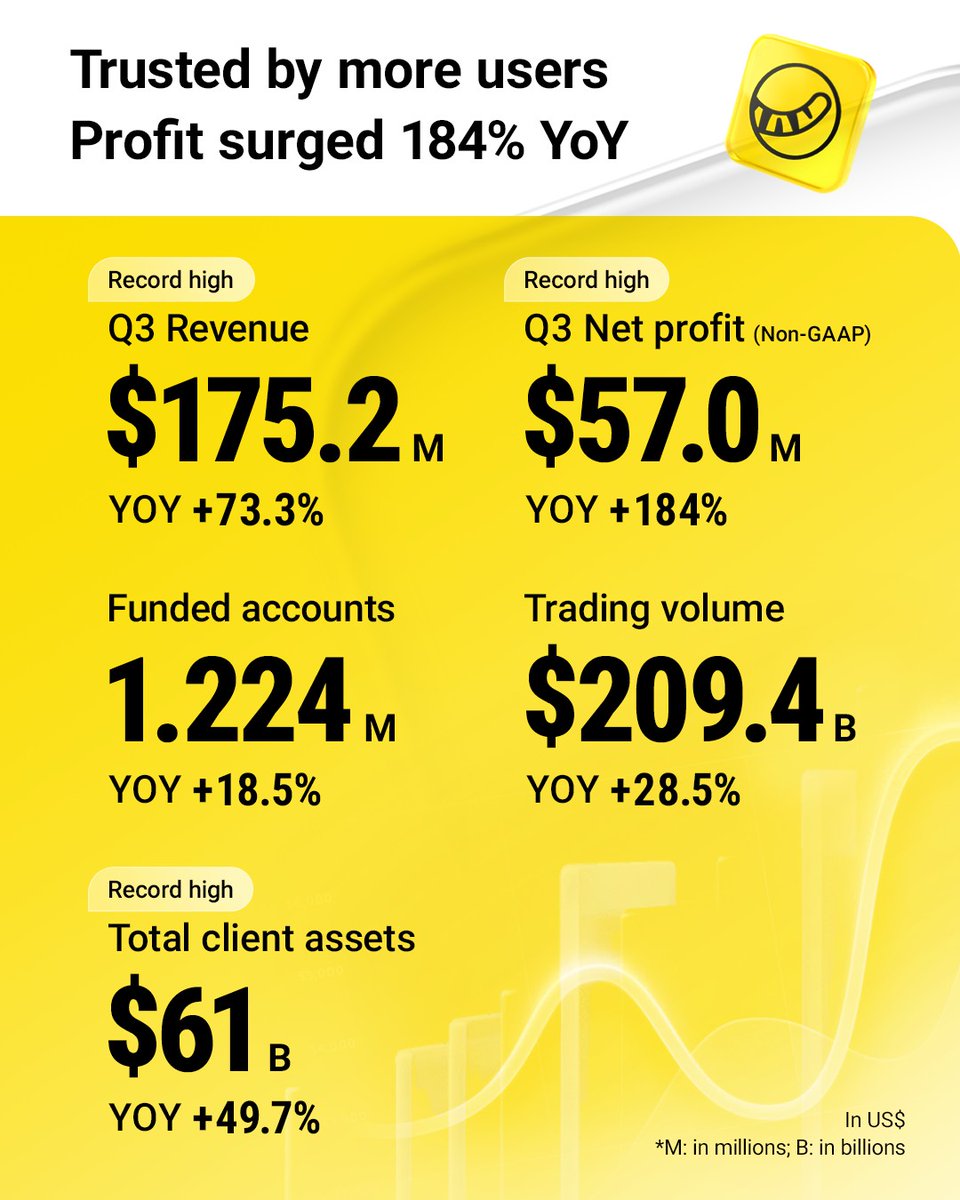

Tiger Brokers $TIGR Q3: ▪️ Revenue +73% ▪️ Net Profit +180% ▪️ Clients Assets +49%

This is what happens when you answer the "tell me about your weakness" question too honestly. PayPal CEO Alex Chriss at Citi's FinTech Conference laid out the challenges so clearly it spooked the market. Here's what he said: 🧵

$PYPL I listened to Alex Chriss talking at the Citi conference I will always be objective despite my position as a shareholder There were some things I did not like; 🔴 THE BAD 1) Consumer pressure is continuing into Q4 across the U.S and Europe with basket sizes showing decreases in the low to middle income groups 2) Branded growth in Q4 will be slower than Q3 due to macro (already known in Q3) 3) Chriss sounded bearish when talking about macro (not a good sign) 4) 15 years worth of incompetence from legacy PayPal is taking longer than anticipated to resolve in relation to integration with merchants on the tech side They are only around 15-20% done (large merchants sorted) but it could take 2+ years to resolve 100% This is the first time that I have heard this and it wasn’t great to hear as an investor This shows just how bad legacy management was at PayPal There was a level of negligence and incompetence which is off the scale and has set the business back years 5) Investment spending was indicated for next year. Whilst I do think this is good and the right thing to do for the long term success of the company, this could pressure margins and feed the “margin compression” narrative 6) Chriss was asked about guidance in relation to EPS and margins. Chriss was a bit vague here and focussed on the point about investing in growth for the future success of the company I would have liked to have seen guidance reaffirmed. With deteriorating macro and now a potential guidance threat, this does not bode well for near to mid term stock performance 🟢 THE GOOD 1) PayPal now has the ability to choose what it does in terms of investing for future growth or to juice the bottom line. This was not the case two years ago 2) Chriss talked about how they are positioning themselves to win in BNPL and Agentic commerce in the future. 3) PayPal is not just an online company anymore, they meet customers everywhere and this will aid growth going forward 4) Venmo will clear $2B imminently way ahead of 2027 guidance. They have only unlocked around a quarter of the ARPA potential and subsequent monetisation of the user base, loads of growth runaway 5) PayPal is positioned to take the Agentic market due to its trusted brand status amongst consumers. This trust will become critical to consumers when using LLMs for purchases and should cement PayPals position as a key player in Agentic commerce 6) PayPal is batting heavy and making moves to lock in decades of future growth. This may require investment, but its short term pain for long term gain CONCLUSION Overall this was a hard listen and il be honest I found it somewhat concerning, particularly on the macro front It’s clear that the things that are going wrong are not in the CEOs control (macro and legacy incompetence) but the turnaround could take a while longer yet This is not what I wanted to hear and I am now reassessing my allocation size going forward I am not selling but I also expect downward pressure in the near term due to the lack of guidance reinforcement for 2026 and macro concerns This is the first time I have not felt bullish in the near to mid term Long term, I am still 100% convinced in the future of the company and its valuation After all, that’s why I felt able to allocate so aggressively (obviously too soon with the benefit of hindsight) But I was not expecting 2026 to be another potential transition year I hope that’s not the case, but Alex did not fill me with confidence on this occasion TLDR: Short to mid term bearish (Macro/legacy incompetence drag) Long term, even more bullish than before This is a bump in the road Not a good day for me and other PayPal shareholders, but I still remain confident in the business fundamentals and that is way more important than price action Not financial advice All thoughts welcome Abuse will not be tolerated, I am In no mood for that today (expect to be insta-blocked)

🦔CoreWeave is spending $310 million on interest expense against just $51.9 million in operating income, borrowing money to pay interest on previous loans. The AI data center company went public in March at $40 per share, peaked at $187 in June, and now trades around $75 while carrying $14 billion in debt. The Problem Microsoft accounts for 67% of revenue but is building its own AI chips and data centers. OpenAI has a $22.4 billion contract but can terminate if CoreWeave doesn't deliver, and is investing in Stargate to supply 75% of its own compute by 2030. Meta signed a $14 billion contract but sold $30 billion in bonds to build its own facilities. All three major customers could become competitors. Nvidia is CoreWeave's investor, customer, and vendor, owning $4 billion in shares while CoreWeave owns 250,000+ Nvidia chips and uses them as collateral for loans at 9 to 15% interest to buy more Nvidia chips. My Take I think CoreWeave shows how the AI infrastructure boom actually works. The company is building data centers for customers who are simultaneously building their own facilities to compete with them. Spending $310 million on interest against $51.9 million in operating income means borrowing to pay interest on previous loans, which isn't sustainable. What stands out is Nvidia being the investor, customer, and chip supplier while CoreWeave uses Nvidia chips as collateral to borrow money to buy more Nvidia chips. Nvidia profits from chip sales without taking on CoreWeave's debt, and this pattern repeats across Crusoe, Lambda, and Nebius, all of which took on debt to buy Nvidia chips and none make money. Hedgie🤗

Dear lord: *OWENS CORNING GUIDES 4Q EBITDA of ~$366M VS. $517M EST What is going on in shelter construction? Yesterday we had $JELD -30% Today we already have $TREX -33% Now add $OC...

Oh my god: *TREX SEES 4Q NET SALES $145M VS 200M EST How dead is home improvement? Or is it just branded home improvement? $TREX

And What Did That Look Like Tactically In His First Months? Alex went on a comprehensive listening tour, meeting with global customers, investors, partners, and leaders. He needed to understand at the ground level what PayPal's secret sauce was, what people wanted to change, and what stakeholders thought was holding them back... "And then at some point you gotta put your stamp on it and you gotta have some conviction, write it down and say - This is the direction we're gonna go."

I have been invested in $PGY for a while and went in very heavy early in the year when the price was $9-$12 and even at the prices we are at now, it still feels like one of those “sleeping in plain sight” fintechs. Pagaya isn’t trying to be another neobank. It’s the AI engine behind the scenes, plugged into banks, fintechs, and auto lenders, helping them say “yes” to more customers without blowing up their risk book. They already power an embedded lending network with 30+ partners including SoFi, Ally, Klarna, and U.S. Bank, plus a growing roster of top-tier banks and auto captives. That’s serious distribution, not a cute pilot. On the funding side, they’ve become an ABS machine, pushing billions in personal loan and auto deals this year alone. Their recent $400–600M and $500M transactions show strong demand from over 70 institutional investors and deepen their capital market rails. They’re also quietly expanding into point-of-sale and BNPL, issuing bonds backed by Klarna loans and positioning themselves as the AI middleman between consumer lenders and Wall Street. If you believe credit is getting sliced, diced, and streamed like data, this is exactly where you want exposure. The tech moat is a massive data network and machine-learning models trained across personal loans, auto, credit cards, and POS. They earn fees on volume while offloading credit risk to investors. Scale improves the models, better models attract more partners, more partners drive more volume. Flywheel 101. Is it risk-free? Of course not. Credit cycles, underwriting quality, and partner concentration all matter. But if you zoom out, $PGY is basically building the picks-and-shovels infrastructure for consumer credit—AI, distribution, and funding pipes all under one roof. That’s why I see it as a potential sleeping giant in fintech. If they keep executing, every new partner, every new ABS deal, and every new asset class quietly increases the odds that their network becomes the default plumbing for how consumer credit gets underwritten.

Kevin. @DeanOwenahfp

1 Followers 220 Following Ex-nuclear engineer hunting hidden atoms. Teaching investors to wield Claude as a junior analyst.

Nancy G @toprakb71833731

16 Followers 1K Following emotionally invested in fictional characters 📖 follow back

Princess Camtoria �... @oOXHTeiJ6nR6dQc

15 Followers 2K Following living softly, screaming internally 💗 follow back always

Martin @martinthbrave

172 Followers 5K Following UK Private investor focusing predominantly on momentum & recovery stocks with large TAM's & strong growth prospects. Mainly US with some Lat Am & SEA.

Gustav @aktieblogg

13K Followers 2K Following Swedish global deep value investor. Building a portfolio of the best nano- to smallcaps I can find. Looking all over the world, but only invests in democracies.

PernixMC @PernixMC

162 Followers 395 Following All-in investor $OPEN leaps ||| Betting all the hard-earned money on the future ||| Let's build a community where us (retail investor) can win the market

Gary X @Gary_veeX

352 Followers 5K Following Educational content only. This reflects my personal opinions and market analysis and is not financial advice.

Jose Manuel @Marmaneu

0 Followers 120 Following

Linda @FaySmith282086

220 Followers 7K Following

Viczmándi Viktória @matthew__sigell

96 Followers 2K Following Head of digital assets research @VanEck_us . PM, VanEck Onchain Economy ETF ($NODE). Disclosures https://t.co/9mcVDf6ckx https://t.co/P6ArBzioMZ

Nate..Endicott @Endlcott1nvests

81 Followers 6K Following Learning about the markets since 2019 | Investor of $PLTR since 2020 | $HIMS investor since 2024 | $NBIS investor since 2025. Always curious

Garcia Capital @GarciaCapg

123 Followers 5K Following QC- @anduriltech | Memes, reposts and opinions are my own.

Popeye Inversor @PopeyeInversor

277 Followers 959 Following 25. Navy Lieutenant. Mechanical Engineer and Law Student. Investor. You set the limit.

Jorge Bartolomé @jorgebartolome

69 Followers 673 Following

Noam @Noam_Mat

230 Followers 880 Following

AktienAkademie @AktienAkademie

228 Followers 421 Following 🛸Information about small cap companies, mostly defence tech, no financial advice, no guarantee that information is correct, do your own research

Matheus Reis @matheuscorreis

226 Followers 3K Following

kaladindz @kaladindz

186 Followers 1K Following “I research, therefore I buy.” - Probably Descartes. Beware because I have no clue of what I'm doing.

Hardik Shah. @AIStockkSavy

117 Followers 2K Following Software Developer | AI-Powered News Insights, Earnings Reports and Analyst Ratings | No Paywalls | Follow for Savvy Insights, Not Advice #AI #StockMarket

TracyJoel @05Na7JfQRx7lt5U

10 Followers 1K Following

Adeline @6fC4f05eRsQKRg

19 Followers 725 Following My hobbies include eating and complaining that I’m getting fat.

Jacqueline @N6jvA92TLOC3Q05

29 Followers 792 Following

Mana1 @profittmana

110 Followers 2K Following Been here since 2011. Navigated cycles, made mistakes, stayed in the game. The mission? $100M is the benchmark. | NFA 🔮

Matteo Muscat @MatteMuscat

1K Followers 3K Following Chief Marketing Officer at Bilbel Capital. Like/ RT ≠ endorsement. Tweets not Financial/investment advice. Views are my own.

GustaveTimothy @ozT8wia5Avxm4lY

41 Followers 1K Following

FibLevelsPro🇺🇸 @Fuorjaw336

50 Followers 2K Following 15-30% Monthly | 2 High-Conviction Stocks.Short-Term Gains: 15-20% in Days/Weeks.DM "JOIN" for WhatsApp Alerts. Live Trade Signals • Market Analysis

Ginale Morin @Ginalemorinfx

245 Followers 4K Following 👨🏾💻 | Helping 9-5ers make money online 🏆 | $0-$90k with Digital Products 🎓 | FREE class this Monday ⬇️

Joel @growthsrapidly

32 Followers 1K Following Proud stock owner of a few growth stocks. Not financial/investment advice.

STOCK MVP @M1ke10947310

169 Followers 6K Following Stock MVP software is designed to save you time when assisting stocks to invest in.

Ron Shamgar @R0nShamgar

296 Followers 7K Following Head of Aussie Equities & Portfolio Manager of TAMIM All Cap/Small Cap Funds. 21 yrs experience in ASX small caps. Investing is my passion. Views are my own.

Kobe @Kobe489092

12 Followers 302 Following

ana ivcia tarot @capitalemploye

48 Followers 856 Following Bienvenido/a, si necesitas ayuda o quieres charlar, contáctame directamente por WhatsApp para cualquier trabajo de hechizos al +447445373876.

Eleni-34 @Eeseeqoo7174

1 Followers 91 Following Don't look for the needle in the haystack. Just buy the haystack! - John Bogle https://t.co/ko0UzPNUW0

Andy @evfcfaddlct

27 Followers 816 Following In the end, investing is about valuation. Get 20% discount for the best valuation tool:

RonnieV @TheRonieVShow

91 Followers 3K Following Full-Time Trader & Investor | 10 Years of Experience I "Where Trading and Investing Meet" | Not Financial Advice

M. V. Cunha.H.|.Perso... @mvcinvesting01

138 Followers 3K Following Long-term investor. BSc in Economics, MSc in Finance. Equity Analyst witha focus on Fundamental Analysis and Valuation. Not a financial advisor.

Bitácora de Valor @bitacoradevalor

3 Followers 65 Following Análisis empresarial independiente, con sesgo value y perspectiva a largo plazo.

.... @madridsecre

565 Followers 7K Following

Aswath iDamodarnn7 @AswathDamodara8

136 Followers 3K Following Fascinated by finance & markets and like writing about them, but teaching is my passion.

Simon Handrahan | MOS... @MoS_Iinvesting

136 Followers 556 Following Author and investor at https://t.co/ET2l2JiXNL

SixSigmaCapital @sixsigmaCaptal

173 Followers 7K Following Individual Investor | Sports Fan | Doctor Opportunistic Investing style Here to learn and share

Clark Square Capital @Accountsaved14

33 Followers 460 Following Global investor. I publish in-depth research on under-the-radar stocks and special situations. Subscribe at https://t.co/Sn2941Zz9E

김수범 @gimsube92299917

34 Followers 715 Following

Gaetano @crux_capital_

51K Followers 522 Following Photonics/Physical AI Company Coverage On Substack https://t.co/6T2naqbkXV

Quality Value Investi... @qualityvalueinv

287 Followers 254 Following Individual investor. Here's my substack: https://t.co/AErPIPfmbH

Papa León XIV @Pontifex_es

16.7M Followers 48 Following Bienvenidos al perfil oficial de Su Santidad el Papa León XIV.

Ltd Eclipse @Ltd_Eclipse

369 Followers 1K Following

Joe @joedab12

8K Followers 406 Following Sold a tech finance co in 2021 and now trade/invest full time. Specialty is finding semi/AI infra inflection points before the breakout. Plenty of receipts.

Fede Sandler @FedexSTi

29K Followers 2K Following Ex-IRO @MercadoLibre & @Nubank. LatAm fintech, capital markets & AI @neuramedia · Professor @utditella · @Forbes_CA columnist · @aspeninstitute Fellow

Investorfile @IFGerryWimmer

3K Followers 248 Following Finding undervalued TSX/TSXV MicroCap stocks early to gain outsized returns: $GSI.V $IQ.V $IFA.TO $STC.TO $ECO.TO $PVT.V $TLA.V $CWL.TO $NVI.V $FRSH.V

P Equity Research �... @pequityresearch

6K Followers 265 Following Research 📃 | PMs open 👇 | Sharing my knowledge & insights with the world 🌍 | Deep dives posted on my substack! 📍

Brian Coughlin @EquityBrian

11K Followers 588 Following Investing, mostly. The longer version is at https://t.co/aVFT25nefY

محمدباقر قا... @mb_ghalibaf

658K Followers 5 Following سرباز امام شهید انقلاب | Speaker of Islamic Republic of Iran’s Parliament

research2discovery @R2Discovery

2K Followers 114 Following Focused on finding great businesses. Concentrated Long Term Investor. Insights Driven. Own opinions, no investment advice.

HFI Research @HFI_Research

114K Followers 90 Following Contrarian Investment Research: Energy (Oil & Gas)

MarketswithMay @marketswithmay

11K Followers 361 Following Opinionated finance commenter mostly posting on the 400+ earnings calls I listen to a Q. I don't give advice. It's your $, do your DD.

NS Investments @NStepmum

769 Followers 1K Following Global value stocks // your favorite contra https://t.co/YBAn6pyphH

Seedy19 @seedy19tron

20K Followers 1K Following Biotech • sometimes not long enough, sometimes not short enough • Tweets are not investment advice

Longview Research @Longviewres

2K Followers 119 Following Focused on AI power. Views are my own. Not investment advice.

Temple 8 Research @Temple_Eight

5K Followers 647 Following Mapping the 2025-2035 AI Build Out. Focus: AI x Macro x Energy Infrastructure. Institutional-grade Intel for Investors. https://t.co/Mro3MmPr0u

Net-Net-Hunter Japan @hiroki1379

2K Followers 83 Following Born in Japan → Study in Japan → Work in Japan Accenture → Freelance → Full time investor

Silicon Salvage @SiliconSalvage

17K Followers 3 Following AI has killed software and tech stocks. Valuations are at multi-decade lows. Stock prices are in the trash. This is a once in a lifetime opportunity to buy fear

Paradis Labs @ParadisLabs

56K Followers 98 Following AI/Semiconductor Analyst & Trader. Thematic investment research. Not financial advice (DYODD).

Ragnarok Research @ResearRagnarok

1K Followers 2K Following Commenting on egregious valuation gaps. Not investment advice.

Jeff Pu @sssjeffpu

34K Followers 47 Following Tech Enthusiast. 20 years tech equity research + industry.

Graham Stephan @GrahamStephan

212K Followers 168 Following Real Estate Investor, Car Enthusiast, 5M+ Subs on YouTube. Newsletter - https://t.co/UnzRcv7mqr Insta - https://t.co/LwD4Qgd2eH

The Hormuz Letter @HormuzLetter

86K Followers 62 Following Iranian. The Middle East through the lens of oil, markets, and money. This is the only account.

Tokyo Deep Value @TokyoDeepValue

34K Followers 9 Following Japanese stocks are the last great deep value trade on earth. Rock solid balance sheets. Monster cash flows. Dirt cheap prices. I find them and buy them

Dimitry Nakhla | Baby... @DimitryNakhla

21K Followers 2K Following Founder & Portfolio Manager | JD 🏛 | Long-Term Investor Focused on Quality Stocks at Reasonable Prices 💵 | Not Investment Advice ‼️

Survival Instinct @SurvivalInstint

101K Followers 32 Following Daily Survival Training, Martial Arts, Self-Defense Videos For Preserving One's Life, Liberty, and Dignity.

Miguel Dabán Baines-... @MDBBolsa

18K Followers 545 Following 👉24Y I 📈 SIL Equity Analyst 👨🎓 M° Bolsa y MMFF por el IEB 📝 MDBbolsa Substack 📘 Partner de Invirtiendo en Alpha https://t.co/IUAo1kekNW

Steve Sweeney @SweeneySteve

149K Followers 6K Following Award-winning, Beirut-based war correspondent/conflict journalist, commentator, filmmaker. Reports from the ground.

Hugo Navarro @HugoNavarroPer2

11K Followers 61 Following PM and writer of Undervalued and undercovered. https://t.co/Z8gNyWJt5M

Patricia Marins @pati_marins64

404K Followers 769 Following . support my work here 👉🏻 PayPal: [email protected] pix: [email protected] join my Substack: @global21.substack.com

David Orr @orrdavid

35K Followers 87 Following I run a hedge fund and an ETF. https://t.co/g9Pxh7mZG2

Joe Value 🕊️ @JoeValue

3K Followers 1K Following Run a concentrated global equities fund. As well as an IFA firm. Nothing here is advice! Podcast interview: https://t.co/XYjdVh7XVr

The Oak Bloke @BlokeOak57182

1K Followers 53 Following I analyse stock investments (mainly UK). My interests range widely, but Mining, O&G, Venture Capital and Special Situations I find most interesting.

Japan Deep Value @JapanDeepValue1

8K Followers 811 Following 60% of all listed stocks in Japan trade below book value. Follow me on a journey to explore. *hint* governance matters. Not giving investment advice.

Stonks Value @DeepValueStonks

6K Followers 156 Following Value investor from Poland running a family portfolio with ~25% CAGR since inception. Not investment advice.

Dirt Cheap Banks @dirtcheapbanks

66K Followers 31 Following Community banks are the last bastion of cheap value in the public markets. I find dirt cheap banks.

Unicorn Hunter 📈 @EUnicornHunter

1K Followers 127 Following I score every stock across 15 KPIs — valuation, growth, profitability, momentum. Full workings. No tips. Just the framework. 📝

Mr Deep-Value @mr_deepvalue

8K Followers 155 Following I help you find cheap stocks to beat the market.

Say No To Trading @SayNoToTrading

20K Followers 188 Following Not a trader, I swear. Just obsessed with capturing lowest cost basis on falling knives, which entails lots of buying and selling. NOT INVESTMENT ADVICE.

Damian Brik @eldaminato

53K Followers 502 Following Economía, Finanzas y Mercados. Entender es más importante que saber. Sin riesgo no hay beneficio. Long term investor.

Liger Cub @realLigerCub

10K Followers 1K Following Long-biased microcap stockpicker. Author of Byron Street Research. Read my disclaimer on each report.

Sebastian Rodriguez @investormdp

201 Followers 648 Following

Giles Capital @GilesCapital

534 Followers 715 Following Value Investing and Trading by Giles Capital. Sign up to our free newsletter here for our analysis & recommendations: https://t.co/F1KyfcN6cI

StockMarket.News @_Investinq

88K Followers 709 Following Covering the biggest moves in the stock market, the headlines making waves, and the trends shaping tomorrow. Not Financial Advice!Trends for United States

You might like