Udara Peiris @UPeiris

A/Prof of Financial Economics @oberlincollege | PhD @UniofOxford | macro-finance | Academic and policy articles on my website | https://t.co/x2CQCJcGRN linktr.ee/upeiris Oberlin, OH Joined December 2011-

Tweets154

-

Followers386

-

Following1K

-

Likes217

@t_holden Interesting paper @t_holden - have you looked at the Malinvaud model? its the simplest rationing model I've come across

As a researcher in the history of economic thought, I found your paper to be exceptionally intellectually stimulating, and I sincerely congratulate you on its publication. Unfortunately, due to a prior commitment, I was unable to attend the presentation in Japan. However, I have heard highly enthusiastic feedback from those who did attend. I am also deeply grateful that you have paid such careful attention to, and generously acknowledged, the contributions of Japanese economists to the theory of equilibrium stability. If I may, I would like to offer a few brief comments from the perspective of a historian of economic thought. Your paper is a remarkable achievement in the tradition of general equilibrium theory. By embedding tâtonnement into a forward-looking dynamic environment with price-setting firms, you provide a compelling rehabilitation of stability analysis and, in many respects, a rehabilitation of Hicks's insights in Value and Capital (1939). However, I wonder whether the paper may be recovering only one Hicks—the young Hicks of Value and Capital—while leaving aside the very different Hicks of his later work. In Value and Capital (1939), Hicks treated prices primarily as adjustment variables within an interdependent market system. From that perspective, your result that forward-looking price setting restores the relevance of Hicksian stability conditions is both elegant and important. Yet in his later writings, especially A Market Theory of Money (1989), Hicks increasingly moved away from the Walrasian conception of price adjustment. He argued that many actual markets operate not through continuous price adjustment but through relatively stable prices that function as commitments between buyers and sellers. In this later Hicksian perspective, a price is not merely a signal of scarcity. It is also a promise. Frequent price changes may undermine confidence, customer relationships, and perceptions of quality. Price stability is therefore not simply a friction delaying adjustment; it is itself part of the institutional structure that makes markets possible. My concern here is not simply the familiar disequilibrium tradition associated with Clower and Leijonhufvud. In those approaches, quantity adjustment typically emerges because price adjustment is incomplete, delayed, or otherwise impeded. The underlying benchmark nevertheless remains a price-adjustment economy. The later Hicks appears to suggest something more radical. Relatively fixed prices may themselves constitute a normal institutional feature of organized markets rather than a temporary imperfection. In such markets, prices are not merely adjustment variables waiting to respond to excess demand; they are commitments that sustain confidence, reputation, and ongoing relationships between market participants. If this is correct, then inventories, delivery lags, customer relations, and other non-price mechanisms are not simply second-best substitutes for missing price adjustments. They are part of the primary adjustment process itself. The question is therefore not how an economy converges when prices adjust imperfectly, but whether many real-world markets should be understood as operating through a fundamentally different logic of coordination. This raises a question about the meaning of “general” in general equilibrium theory. Your model incorporates sticky prices, but the underlying role of prices remains fundamentally Walrasian. Prices are still the primary adjustment variables; stickiness only affects the timing of adjustment. The economy ultimately remains a price-adjustment system. This is true even when prices are sticky in the Calvo sense. By contrast, the later Hicks seems to suggest that many real-world markets may be better understood as operating under relatively fixed prices, with much of the adjustment occurring through quantities and other non-price mechanisms. Inventories, delivery schedules, customer relationships, reputation, and other institutional arrangements absorb shocks that Walrasian models assign to prices. If this interpretation is correct, then the issue is not merely whether prices are flexible or sticky. The deeper issue concerns the social ontology of prices themselves. In the Walrasian tradition, prices are primarily signals. In the later Hicksian tradition, prices are also commitments. The distinction matters because a commitment-based pricing system may generate stability through mechanisms fundamentally different from those analyzed in tâtonnement models, however sophisticated. Therefore, while your paper may successfully restore stability theory within a Walrasian framework, one may still ask whether the later Hicks's fixprice economy represents a different class of market order altogether—one whose stability cannot be reduced to price dynamics alone. From this perspective, the issue is not whether a Walrasian price-adjustment economy can be made stable. Your paper shows that it can. The question is whether such an economy exhausts the relevant notion of generality in the analysis of market coordination. In that sense, the question is not whether Hicks is back, but which Hicks has returned.

Excited to FINALLY release toughest+most rewarding paper I've worked on... ….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)... Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯ 🧵

📢 Macro Theory with Measured Expectations (with Roth, Wiederholt, Wohlfahrt)📢 The Lucas critique says policy evaluations based on historical correlations can fail because policy changes alter expectation formation. We propose a way to address this: measure expectations under alternative policy scenarios. Below, I quickly describe 4 key results that emerge from this approach. Details in the paper👇 ralphluetticke.com/files/LRWW_202…

I will be out of the country this summer, but I have addressed similar question many times in simpler models so the lesson may not translate. I look forward to reading this paper and discussion that follows. In my experience, approximations tend to work surprisingly well. However, there are two important considerations, both drawn from my paper with Sanjay Singh (2019): ideas.repec.org/p/nbr/nberwo/2… 1. When you consider a nonlinear version of the model, make sure the nonlinear model does not have implausible properties that the modeler originally intended to eliminate through linearization. Examples include quadratic investment adjustment costs or costs of changing prices. In a nonlinear setting, it rarely makes sense to assume a quadratic function; from a theoretical point of view, such an assumption is highly implausible. There are plenty of functions that are equivalent up to first order but are theoretically more appropriate. 2. The “deeper” point made in the paper, though I do not think it is fully appreciated—or perhaps people simply disagree—is that you need to re-parameterize the model when evaluating the nonlinear counterpart to the linearized version and do policy analysis. More precisely, we typically parameterize our models conditional on the solution method—for example, most commonly by using Bayesian methods on log-linearized models. I do not think it makes sense to take parameters estimated from a linearized characterization, put them into a nonlinear version of the model which has particular functional forms which often just show up as elasticities to a first order, and then ask whether the answer to the policy question changes. You need to re-estimate the nonlinear model on the data and then ask the same question you asked before. The parameterization/estimation are conditional on how the model is solved (og linear or non-linear). Once this is done, I have found that what initially look like major differences often turn out to be small. That said, I have not done similar comparisons involving more complex objects, such as time-varying cross-sectional distributions. I am therefore curious to read the paper and the discussion that follows. But the general point: There is a family of nonlinear models generating the same log-linear approximation. Which member of this nonlinear family of models you pick obviously matter. To have that model speak to the same policy question as the approximated model you better make sure it fits the data along exactly the same dimensions.

📢 New paper w/ @GregWKaplan 🧵1/10 How small is “small” for local-linear methods to deliver reliable answers in heterogeneous-agent models of fiscal stimulus? Our answer: very small.

Excited to FINALLY release toughest+most rewarding paper I've worked on... ….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)... Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯ 🧵

Alternative scenarios often proved more accurate than the baseline forecast. New #FEDSPaper catalogs 1,265 'what-if' exercises from 1968-2020, tracking how Fed staff prepared for demand shocks, supply disruptions, and financial crises. federalreserve.gov/econres/feds/a… #FedResearch

100 years ago today: violation of the No Ponzi Game condition

It is an absolute pleasure to release this new work, joint with the great Emmanuel Farhi and Alan Olivi: "Price Theory for Incomplete Markets" (the title is a wink at my alma mater). At long last, as it has been a very long haul. drive.google.com/file/d/1yi8p5z… A brief thread 1/n

New #FEDSPaper: The Causal Effect of Debt on Interest Rates: federalreserve.gov/econres/feds/t… #EconTwitter

Studying how central banks should respond to commodity price shocks by showing that optimal monetary policy depends critically on the economy’s commodity exposure, from @td_econ, Michael McLeay, Silvana Tenreyro, and Enrico D. Turri nber.org/papers/w35164

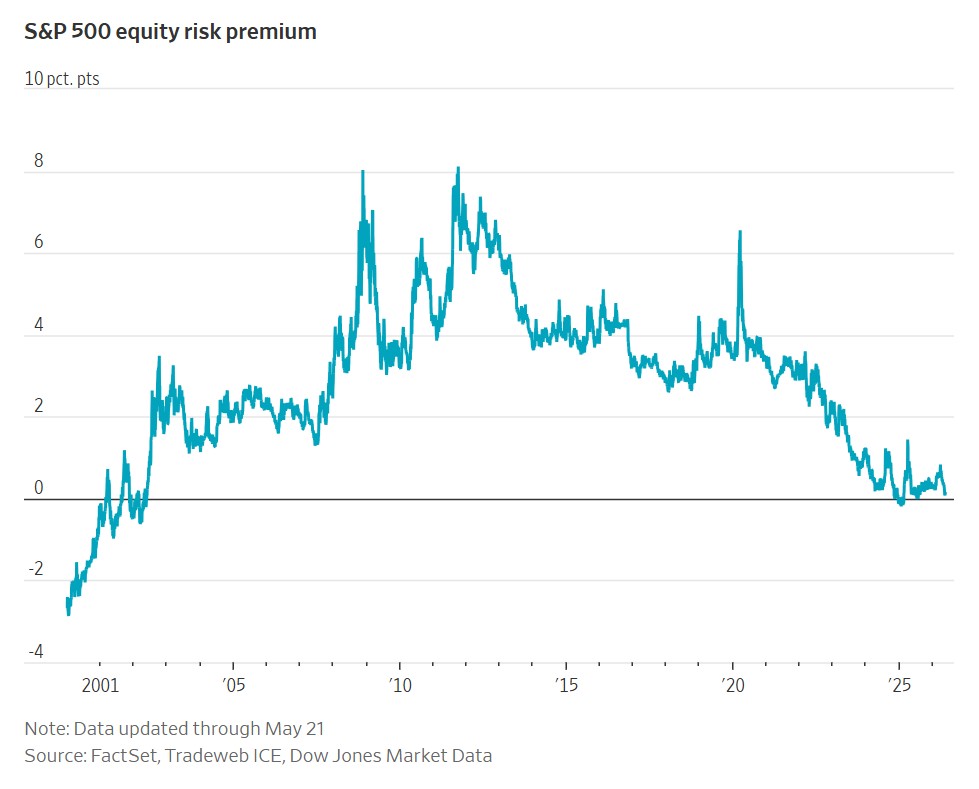

If one wants to do this, compare P/E to TIPS yield, not nominal yield. Nominal yield is higher when expected inflation is higher. P/E is not affected by inflation.

This chart comes the @WSJ article on “The Risk Premium for Holding Stocks Over Bonds Is Vanishing: Gap between market’s earnings yield and bond yields has narrowed, a measure that has at times predicted subpar stock returns.” What investors should do about this is far from

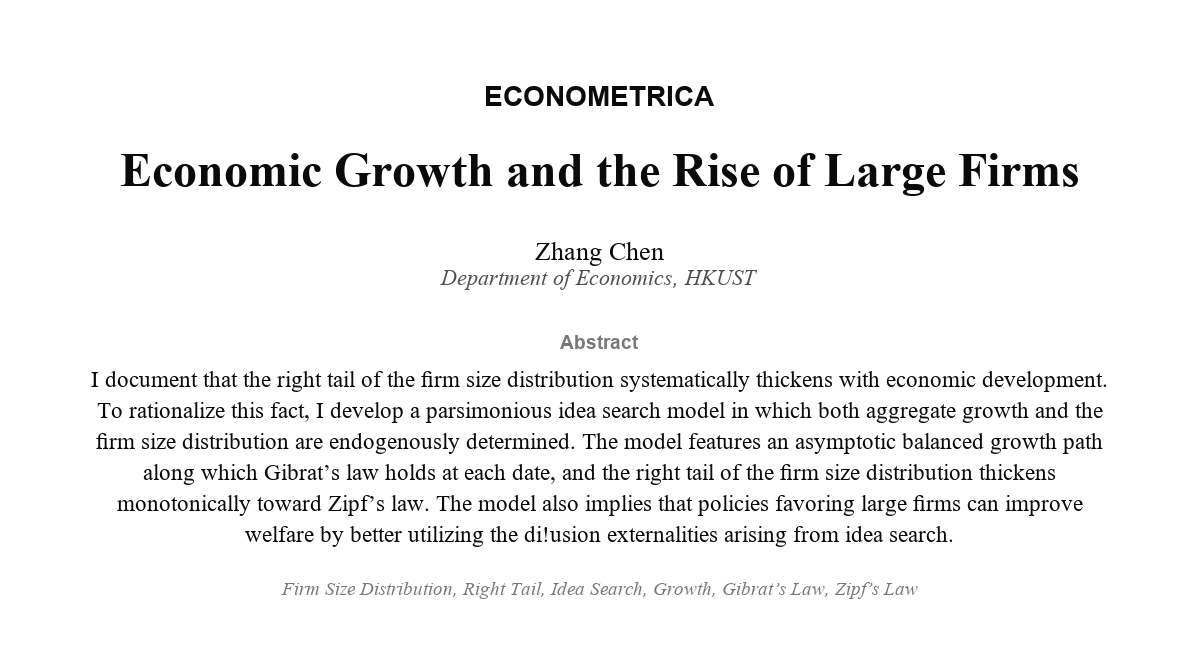

Why do richer economies have more very large firms? This paper shows that the upper tail of the firm size distribution thickens as economies grow. A model of idea search explains why, showing how growth itself can produce rising concentration. econometricsociety.org/publications/e…

A Curious Fact from the History of Economic Thought: The Phillips Curve was first discovered by Irving Fisher, not A.W. Phillips. Fisher was the first economist to conduct a statistical study and observe a trade-off relationship between inflation and unemployment in a 1926 paper. For comparison, Phillips' paper, which gave rise to his famous curve, only appeared in 1958! The Journal of Political Economy even published a little-recognized retraction of this historical error in 1973. Link: cooperative-individualism.org/fisher-irving_…

Hagedorn's results on price level determination are incredibly important. They are a true third theory of the price level to go along with the active monetary policy approach and the FTPL. (No, Hagedorn's theory is not a special case of FTPL.) It's a tragedy that he isn't around to see them published. Of course, none of the three approaches are perfect, but showing that options A and B are not the only possibilities is a massive contribution, deserving of a top 5.

Super interesting! "A Demand Theory of the Price Level" by Marcus Hagedorn (The paper was submitted to the International Economic Review posthumously. Sadly, Marcus Hagedorn passed away too soon.). "Heterogeneous agent incomplete markets models offer a new perspective on price

Sad news: mathworks.com/company/aboutu… Rest in peace, Cleve Moler. Thank you for all your work. #Matlab @MATLAB @MathWorks

Smartphones are not the explanation for the recent decline in fertility. Instead, they are an accelerator of deeper forces already at work. Let’s start with the facts. Fertility is falling almost everywhere: in rich, middle-income, and poor countries; in secular and religious countries; and in countries with high and low levels of gender equality. The decline accelerated around 2014. So, no country-specific explanation will work unless you are willing to believe that 200 distinct country-specific explanations arrived at roughly the same time. Smartphones look like the obvious candidate: the first iPhone was released in 2007, and global adoption has been astonishingly fast. Economists understand the first major decline in fertility in advanced economies, from 6 or 7 children per woman throughout most of human history to about 1.8, that occurred between the early 1800s and roughly 1970, well before smartphones. The main drivers were a sharp fall in child mortality (effective fertility was rarely above 3 and often close to 2) and the shift from a low-skill, rural agrarian economy to a high-skill, urban industrial one. We have quantitative models that fit these facts well. Country-specific factors mattered too, of course. Proximity to low-fertility neighbors accelerated Hungary’s decline, while fragmented landowning structures accelerated France’s. But these were second-order mechanisms. This is also why most economists long considered Paul Ehrlich’s doom scenarios implausible. We forecast that fertility in middle- and low-income economies would follow the same path as in the rich, probably faster, because reductions in child mortality reached India or Africa at lower income levels (medical technology is nearly universal, and most gains come from handwashing and cheap antibiotics, not Mayo Clinic-level care). Much of what we see in Africa or parts of Latin America today is still that old story. But in the 1980s, a new pattern appeared. Japan and Italy fell below 1.8, the level we had thought was the new floor. By 1990, Japan was at 1.54 and Italy at 1.36. This second fertility decline began in Japan and Italy earlier than elsewhere, driven by country-specific factors, but the underlying dynamics were widespread: secularization, an education arms race, expensive housing, the dissolution of old social networks, and the shift to a service economy in which women’s bargaining power within the household is higher. The U.S. lagged because secularization came later, suburban housing remained relatively cheap, and African American fertility was still high. U.S. demographic patterns are exceptional and skew how academics (most of whom are in the U.S.) and the New York Times see the world. My best guess is that, without smartphones, Italy’s 2025 fertility rate would be about 1.24 rather than 1.14. I doubt anyone will document an effect larger than 0.1-0.2. Italy was at 1.19 in 1995, not far from today’s 1.14. The TFR is cyclical due to tempo effects, so I do not read too much into the rise between 1995 and 2007 or the decline from 1.27 in 2019 to 1.14 today. The direct effect of smartphones is not zero, but it is not, by itself, that large. Where social media, in general, and smartphones, in particular, matter is in the diffusion of social norms. What would have taken 25 years now happens in 10. Social media are not the cause of fertility decline; modernity is. But they are a very fast accelerator. That is why social media are a major part of the story behind Guatemala (yes, Guatemala) going from 3.8 children per woman in 2005 to 1.9 in 2025. Without them, Guatemala would also have reached 1.9, just 20 years later. Modernity, in its current form, is incompatible with replacement-level fertility. By modernity, I do not mean capitalism: fertility fell earlier and faster in socialist economies than in market economies. Socialist Hungary fell below replacement in 1960, and socialist Czechoslovakia in 1966 (both experienced small, short-lived baby booms in the mid-1970s). By modernity, I mean a society organized around rational, large-scale systems and formalized knowledge. Countries will not converge to the same fertility rate. East Asia is likely stuck near 1, possibly below, given its unbalanced gender norms and toxic education systems. Latin America faces the same gender problem plus weak growth prospects, so I expect something around 1.2. Northern Europe has more egalitarian family structures and might hold near 1.5. The very religious societies are probably the only ones that will sustain 1.8. All of this could change with AI or changes in population composition. We will see. But on the current evidence, deep sub-replacement fertility is the “new new normal.” Unless we reorganize our societies, better learn to handle it as best we can.

Clearly very behavioral, but even in the digital age I have a utility kick from seeing papers finally in "print." (w. @SBryzgalova and Jiantao Huang) doi.org/10.1111/jofi.7…

🚨 "Consumption in Asset Returns" (w. @SBryzgalova & Jiantao Huang) forthcoming @JofFinance We use asset returns to uncover the elusive dynamics of consumption. Turns out, financial markets know a lot about future consumption—and it matters for both macro & asset pricing🧵👇1/n

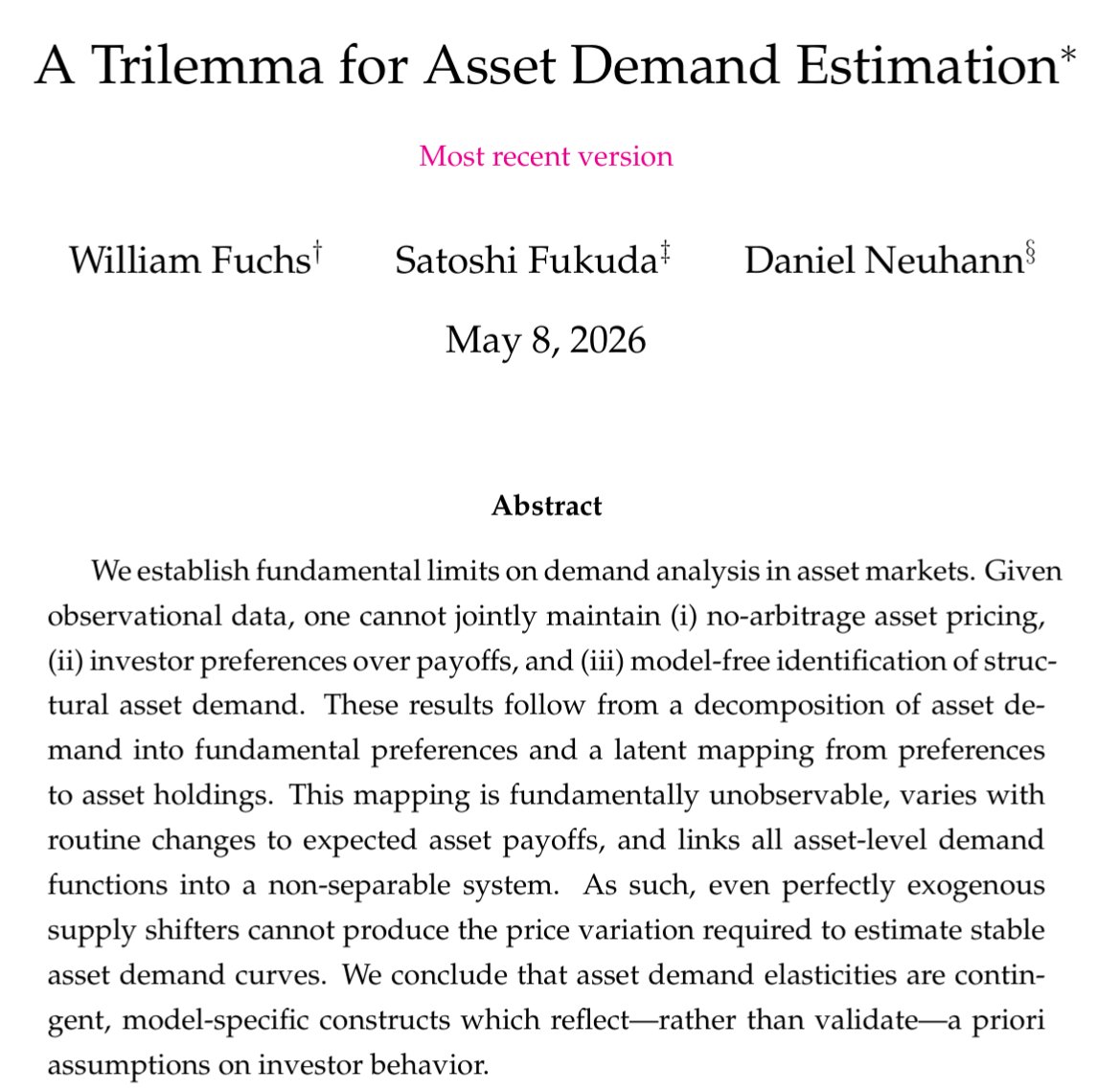

New paper by Fuchs et al pushes critique of asset demand estimation even further. With observational data, you can't simultaneously maintain no-arbitrage pricing, investor preferences over payoffs, and model-free identification of asset demand.

Robert Czech @RobertCzech8

241 Followers 294 Following Researcher at the Bank of England. Personal views only.

Jhon González @JhonEconomics

55 Followers 821 Following Labor economics, macroeconomics, inequality, and development. Ph.D. in Economics @LeMansUniv. MRes @PSEinfo, @LeMansUniv. Maitrise @TSEinfo. Economist @UdeA

Khanh Le @khanhlehg

2 Followers 27 Following

bijoyetri @Bijoyetri4

1K Followers 7K Following PhD-ing @UWSoc | previously @csbcashoka & @JPAL_SA | law, policy, trust, institutions, causality & measurement | views my very own | rt ≠ endorsement

Auyon Siddiq @auyonomous

251 Followers 416 Following Associate Professor @UCLAAnderson. Market design, digital platforms, AI. @UCBerkeley PhD; secretly Canadian.

Col. Cinco Hamilton @cincohamilton1

83 Followers 5K Following Col. Cinco Hamilton USAF Fighter Test Pilot Former Commander, 9th Ops Group Committed to the mission

Roberto Steri 🇺�... @steri_roberto

1K Followers 812 Following Funny Guy, Assistant Professor of Finance, Never Getting Bored

Miles Kimball @mileskimball

21K Followers 3K Following Eaton Professor of Economics at the University of Colorado and blogger on economics, politics, religion & happiness

Ishika sharma @ishikasharma253

180 Followers 322 Following Exploring the intersections of real estate tech and giving back. Always looking to connect learn and travel Life’s better with meaningful conversations

Giulio Tarquini @TarquiniGiulio

170 Followers 556 Following Research Fellow, Macroeconomics @SapienzaRoma | Έτσι, δεν γνωρίζω

Ryan Israelsen @israelsen

2K Followers 2K Following Finance Professor at Michigan State University @MSUBroadCollege | @MichiganRoss PhD | @HuntsmanSchool Econ | @AmbasciataUSA alum

Rajiv Sethi @rajivatbarnard

6K Followers 4K Following Economics | Barnard | Columbia | Santa Fe Institute | https://t.co/77HCz9cT5R | https://t.co/CbhdzYPN5q | https://t.co/FfwOsUBooJ

Chanik Jo @jo_chanik

1K Followers 887 Following Assistant Professor of Finance at CUHK working on fun stuff in asset pricing, household finance, and behavioral finance. @UofT PhD

Marco Garofalo @mar_garofalo

346 Followers 910 Following Incoming Assistant Professor of Finance @umsbe Ex-@bankofengland PhD @OxfordEconDept ⚽️ Long-suffering AS Roma fan 🇮🇹🇳🇱🇪🇺🇬🇧

V Kumarage @VKumaraewru

48 Followers 1K Following

Ivan T Ivanov @ivan_t_ivanov

984 Followers 1K Following

Lidia Cruces @Lidia_Cruces_

975 Followers 754 Following AP at Goethe University Frankfurt. Macroeconomist interested in Gender, Family, and Labor Economics (among others)

Lukas Verling @LukasVerling

2 Followers 36 Following Student Athlete @ Oberlin College | Financial Economics & Data Science

A @calvo_fairy

145 Followers 645 Following Monetary Policy, Labor, IO and Tennis Enthusiast. Mythical creature who arrives according to a Poisson process. Todo a título personal. 🇲🇽🎾

Motoaki Takahashi @takahashi_xcx

956 Followers 942 Following Assistant Professor of Economics at the University of Osaka. Spatial economics & international trade.

Pascal Meichtry @p_meichtry

572 Followers 609 Following Research Economist @banquedefrance | PhD in Economics @heclausanne | Previously @bankofengland @SNB_BNS | Macro • Monetary • Policy | Views are my own

Mary @Maryd9k7

30 Followers 2K Following 1k followers 100 following..please if you are interested in me please contact me on my Zangi app number 7208671974.or my email address [email protected]

Xiaojie Liu @XiaojieLiu1993

518 Followers 977 Following Bates White; Northwestern Kellogg econ PhD; Sciences Po master; Interested in business cycle and growth; Website: https://t.co/k8IGysOd0x

Simon Soki Hong @SimonHon49

74 Followers 105 Following Econ phd @warwickuni | researcher @bankofengland 🇰🇷 All views are my own.

Riccardo Degasperi �... @RicDegasperi

480 Followers 551 Following Economist @bancaditalia. Previously Econ PhD candidate @warwickuni and PhD Trainee @ecb.

Todd Jones 🦊 @toddrjones

15K Followers 2K Following Econ professor, @msstate, @CESifoNetwork, @iza_bonn | Applied micro, econ of ed, cartography | Alum @USUAggies, @Cornell | Latter-day Saint | Dad x 4

Dennis Essers @DennisEssers

683 Followers 452 Following Economist @NBB_BNB_NL & researcher @IOBUA. Hyped about international economics, sovereign debt, EMs, exotic cuisine & loud techno bass. Personal views. COYR🔴⚪️

Akib Khan @akib_kn

3K Followers 4K Following @hoss_sse @handels_sse ex-@EconomicsUU @WorldBank @IDinsight @BRACJPGSPH @poverty_action @The_IGC @icddr_b; human capital, immigration, experiments; 🇧🇩 🇸🇪

Roberto M. Billi @Roberto_M_Billi

974 Followers 1K Following Economist @riksbanken @RiksbankRes. Views are my own.

Michael Wulfsohn @michaelwulfsohn

218 Followers 623 Following DPhil candidate, Economics (int'l macro finance), @UniofOxford. Actuary. Interests: economics, global governance, development, AI, research, cryptocurrency.

Marco M. Aviña @marcomavina

1K Followers 1K Following PhDing @Harvard_GovDept---I study: class/identity in elections & public opinion; diversity, inequality, & exclusion (D.I.E.); and metascience | 🇲🇽🇨🇦🏳️🌈

Reviewer3 @reviewer3com

2K Followers 2K Following Multi-agent peer review trusted by thousands of researchers.

Pascal Paul @pascalpaul

852 Followers 476 Following Economist @sffed researching links between finance, monetary policy, and the macroeconomy. All views are my own.

Annamaria Lusardi @oshaan63

18 Followers 337 Following @Stanford 's @SIEPR & @StanfordGSB . Previously, University Professor at @GWtweets & Prof. at @Dartmouth . Working on finlit & personal finance. Founder o

Wendy @Torrance756902

5 Followers 85 Following Clear-headed and independent, rational and insightful; focused on the self, and detached from gain and loss.

Swapnil Singh @econswapnil

463 Followers 2K Following Principal Research Economist, Bank of Lithuania/CEFER. Tweets do not represent the official views of my employer.

Manoel Bittencourt @Het_Agents

705 Followers 2K Following Economist (macro & political economics) @ UPretoria | Ed board: Journal of Public Finance & Public Choice, & Journal of Development Perspectives | Views my own

Sebastián Fanelli @Seb_Fanelli

242 Followers 510 Following Associate Professor of Economics at @CEMFInews | Research affiliate at @cepr_org

Frantisek Masek @Masek_F

1K Followers 2K Following Economist in the Research Division at @CNB_cz. PhD from @SapienzaRoma. Previously @ECB_Research, @NBS_sk and visitor at @UChicago and @tu_wien. Views mine only.

Big daddy @Bigdaddyz12344

4 Followers 217 Following

Naoki Yago @naoki_yago

733 Followers 409 Following English Account (Japanese: @NaokiYago) / Lecturer @UniofReading @HenleyBSchool @icmacentre / PhD @Cambridge_Uni / International Macroeconomics and Finance

Thomas Piketty @PikettyWIL

249K Followers 21 Following Compte officiel de Thomas Piketty, professeur @EHESS_fr & @PSEinfo, codirecteur https://t.co/lmi0paMm42, https://t.co/MOOSh5R7mW, https://t.co/lqGLTUNNgx

Oberlin Men's Lacross... @yeo_mlax

1K Followers 176 Following Home of the Oberlin College Men's Lacrosse Team 📸 Instagram @Yeo_mlax ~ Recruit Questionaire Link ~ https://t.co/iDAoYnpLCO

Oberlin WBB @Yeo_WBB

1K Followers 335 Following Official Twitter account of Oberlin College Women’s Basketball | Instagram: yeo_wbb

The Oberlin Review @oberlinreview

2K Followers 843 Following The newspaper of record for Oberlin College and the city of Oberlin, Ohio.

Oberlin Men’s Baske... @Yeo_MBB

2K Followers 382 Following Follow the Oberlin Men's Basketball program for updates on alumni events, rosters, schedules and general info

Oberlin Football @Yeo_Football

14K Followers 128 Following Official Twitter account of Oberlin College Football #GoYeO

Oberlin Baseball @Yeo_Baseball

2K Followers 329 Following Oberlin College Baseball -- NCAA DIII -- Proud member of the NCAC -- Instagram: yeo_baseball

Oberlin College @oberlincollege

8K Followers 280 Following This account has been archived. Please follow us on Instagram or visit our website at https://t.co/GpwuTM6ZdO.

alan rusbridger @arusbridger

204K Followers 5K Following Ex-Editor in chief @Guardian,@Prospect_uk. @OversightBoard. https://t.co/2gU8YUIAH6. Speaking: [email protected] Also at @arusbridger.bsky.social

Alejandro Vicondoa @ale_vicondoa

788 Followers 792 Following Macroeconomist @IE_UC | PhD in Economics @EuropeanUni

Robert Czech @RobertCzech8

241 Followers 294 Following Researcher at the Bank of England. Personal views only.

Marshall Steinbaum �... @Econ_Marshall

41K Followers 2K Following Assistant Professor of Economics, University of Utah. @jainfamilyinst Senior Fellow, Higher Education Finance. Views my own. That said, Free Palestine.

Rigissa Megalokonomou @rmegal

2K Followers 708 Following Assoc. Prof. in Economics at Monash University #monashbusiness, labour, education, gender, @CESIfonetwork affiliate, PhD:@warwickecon, Mother, 🇬🇷 🇦🇺

University of Oxford @UniofOxford

1.1M Followers 1K Following Welcome to our official account 👋 Follow for the latest news, research and updates about life at Oxford.

Gus Hurwitz @GusHurwitz

3K Followers 1K Following Senior Fellow and Academic Director, U.Penn Center for Technology, Innovation, and Competition; Director of Law & Econ Programs @ ICLE

Juan Antolin-Diaz @JuanAntolinDiaz

2K Followers 1K Following Assistant Professor of Finance, @MITSloan. Madrid - London - Boston

Zoe Zhang @QianxueZhang

2K Followers 293 Following Economist. Assistant professor @UTokyoGraSPP. PhD @warwickecon. I work on international trade, growth and innovation.

Jhon González @JhonEconomics

55 Followers 821 Following Labor economics, macroeconomics, inequality, and development. Ph.D. in Economics @LeMansUniv. MRes @PSEinfo, @LeMansUniv. Maitrise @TSEinfo. Economist @UdeA

Anderson M Teixeira @AndersonMTeixe1

302 Followers 2K Following Economist, Associate Professor of economics at UFG/Brasil. Likes: , Economy, Science and soccer! @grêmio!

Saloni @salonium

36K Followers 2K Following Co-founder & editor @WorksInProgMag. Writer, Scientific Discovery. Podcaster, Hard Drugs. Advisor, @coeff_giving. // Prev @OurWorldInData. 🏳️🌈

Michal Szkup @MichalSzkup

40 Followers 54 Following Associate Professor of Economics at University of British Columbia @ubcVSE | International Economics and Economic Theory | Economics PhD from @nyuniversity

Emiliano Luttini @EmilianoLuttini

87 Followers 271 Following Father of Constantino and Zoe. Economist. Italian-Argentine.

Isaac Baley @isaacbaley

2K Followers 1K Following Economics & Vermouth Mexico City -- Brooklyn -- Barcelona @econ_empresaUPF, @CREIResearch, @bse_barcelona, @cepr_org Alumni from @ITAM_mx and @NYUFASEcon

James Graham @J_Meanwell

1K Followers 709 Following Senior Lecturer in Economics, University of Sydney (@USydneyEcon). Research on macroeconomics and housing. Editor, New Zealand Economic Papers (@NZeconpapers).

Felix Tintelnot @FelixTintelnot

3K Followers 334 Following Associate Professor of Economics at Duke University. Dad.

Lawrence Katz @lkatz42

23K Followers 824 Following Economist studying labor markets, inequality, and economics of social problems

Paolo Piacquadio @pgpiacquadio

820 Followers 430 Following Associate Professor @HSGStGallen, StG2018 VALURED @ERC_Research #H2020. Interests: #welfarecriteria, public economics, justice, fairness, and taxation.

Xavier Sala-i-Martin @XSalaimartin

482K Followers 558 Following Author of "Economia de la IA". Professor at Columbia University. I block trolls (especially Florentinians), abusers and would-be censors. No exceptions.

Barbara Biasi @BarbaraBiasi

18K Followers 1K Following Econ Prof @YaleSOM. I mostly tweet about education and sometimes reply to random threads in Italian. Born&raised in Monopoli (ITA). Mom of 3.

Treb Allen @TrebAllen

4K Followers 857 Following Distinguished Professor of Economics and Globalization

Mathilde Muñoz @MathildeMunoz

5K Followers 688 Following Studying globalization and tax competition @berkeleyecon

Emily Nix @EmilyNix100

13K Followers 2K Following Labor economist and professor @USC @USCMarshall. NOLA born and raised, UNC @MoreheadCain BA and Yale PhD educated. Views are my own.

Matt Lowe @hmmlowe

5K Followers 1K Following 🇬🇧 Assistant Professor of Economics @UBC. Interested in devo, PE, behavioural, and sweet foods. R2: ''high on cuteness and low on depth''

Sydnee Caldwell @SydneeCaldwell

4K Followers 1K Following Labor economist. Assistant professor @BerkeleyHaas (EAP) & @BerkeleyEcon

Sergio Ocampo Díaz @socampdi

2K Followers 1K Following Econ Assistant Professor @WesternU| Previously at @UniOslo, @IDB_Research, @BancoRepublica | PhD @UMNews | Economista @JaverianaEcon.

Nathaniel Hendren @nhendren82

11K Followers 641 Following Professor of Economics at MIT. Co-Director of Policy Impacts (https://t.co/57eyCxxbj4) and Opportunity Insights. Co-Lead Editor of the JPUBEC (He/him/his)

Oliver Kim @oliverwkim

7K Followers 1K Following Development economist, working on economic growth at @coeff_giving. PhD @berkeleyecon, AB @harvard. Views my own.

Thomas Bourany @TBourany

2K Followers 1K Following Postdoc @columbia_econ🦁 AP @EIEF_Rome🏛 PhD @UChi_Economics Macro📈/Climate🌱/International Trade🌎 Alumn @sciencespo📖 @Sorbonne_Univ_📊 From Paris🍷🇫🇷🇪🇺

André Diegmann @AndreDiegmann

128 Followers 208 Following

Benjamin Schoefer @Schoefer_B

4K Followers 79 Following Economics professor at UC Berkeley. 🇺🇸🇪🇺🇩🇪 https://t.co/W7yyfR1fuq

Frances 'Cassandra' C... @Frances_Coppola

105K Followers 5K Following Professional writer, speaker and singer. Author of The Case for People's QE (Polity). Slowly writing The Absolute Essentials of Banking (Routledge). Autistic.

Nick Pretnar @nickpretnar

879 Followers 3K Following Economist | Focusing on growth and time use | PHD from @CarnegieMellon | Asst. Director LAEF @UCSB | Incoming Asst. Prof. University of Austin Texas 🌈

Juan Llavador Peralt @LlavadorPeralt

279 Followers 1K Following

Roger E. A. Farmer @farmerrf

15K Followers 551 Following Roger Farmer's Economic Window. Professor of Economics, Warwick University and Distinguished Professor of Economics UCLA.

田中秀臣 @hidetomitanaka

87K Followers 622 Following 経済学者。文化放送「おはよう寺ちゃん」毎週火曜出演、連載:産経ニュース(寄稿隔週)、Newsweek日本版 等。『週刊新潮』に書評寄稿。ここでの発言は個人的なもので、所属する機関とは関係は一切ありません。ご依頼は、hidetomitanaka×https://t.co/Mr4k27qliV まで(×を@に代えて)お送り下さいYou might like